Portfolio-Level Early Warning System

CoT portfolio-level early warning: extremes, crowding, squeeze/exhaustion, composite stress index.

Gemini Summary

Signal Summary:

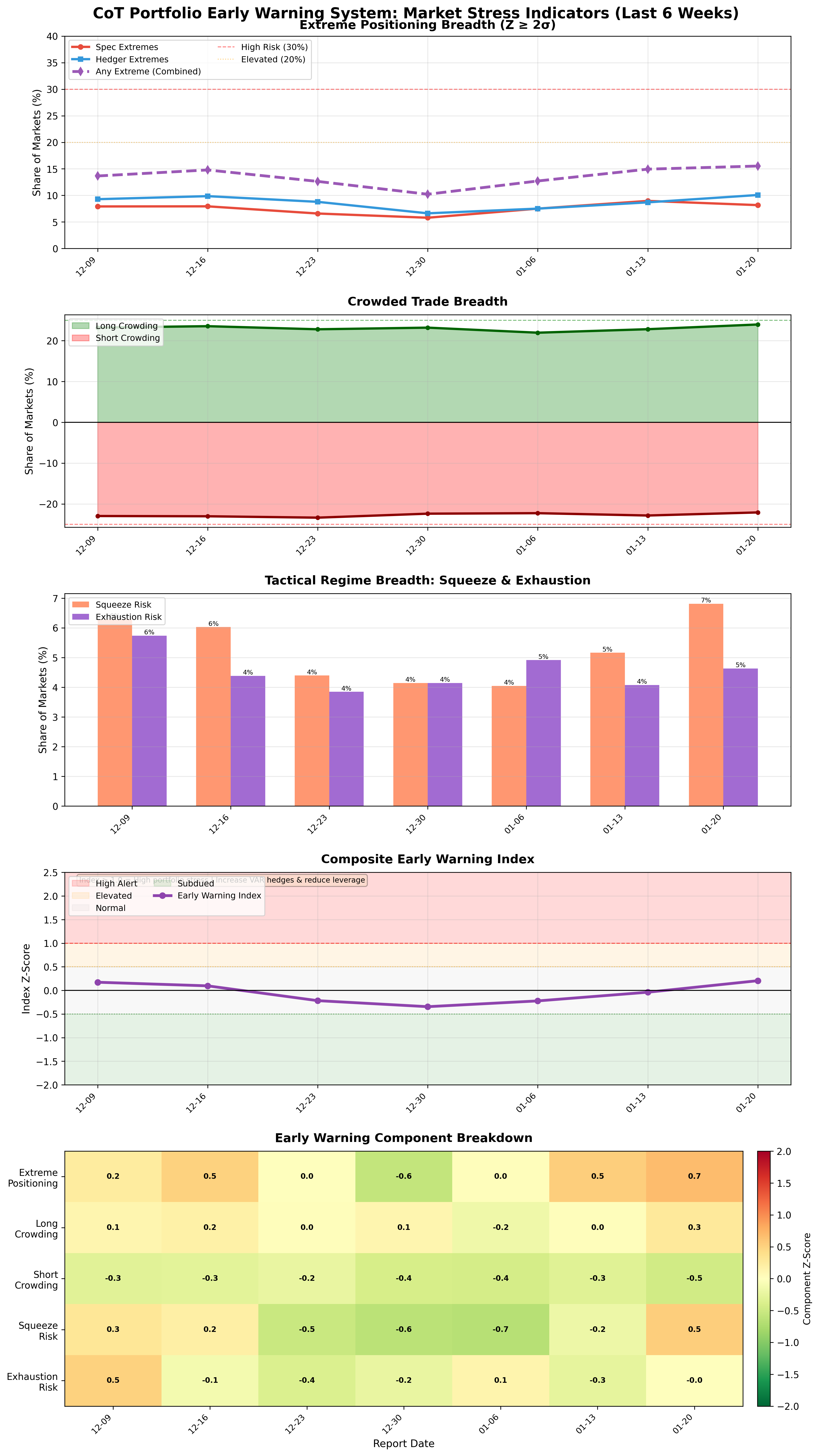

- Configuration statement (mandatory): Given an any extreme share z-score of 2.37 and a speculator extreme z-score of 1.12, this setup aligns with Range-biased price paths and Normal volatility, where the dominant risk is Mean reversion, not Trend continuation. (1)

- The signal is currently in a Normal regime, though the index value of 0.4689 is rapidly approaching the Elevated threshold. (1)

- Conviction Band: Medium; Interpretation Confidence: High Confidence; Internal Conflict Flag: No. Signal Stability Assessment: Deteriorating; Threshold Proximity: Near; Revision Sensitivity: Unknown.

Methodology Applied:

- Regime thresholds define "Normal" market functioning between index values of -0.5 and 0.5. (1)

- Rising index values represent a transition toward risk-off conditions, trend exhaustion, or potential deleveraging. (1)

- Extreme positioning z-scores (speculator and hedger) serve as the primary quantitative inputs for systemic instability. (1)

- Portfolio-Level Early Warning System: Latest observation dated 2026-03-17. (1)

Key Dynamics:

- The primary driver is the sharp spike in "any extreme share z-score" to 2.37, indicating broadening positioning stress across markets. (1)

- Speculator extremes have surged (z=1.12), while hedger extremes are also elevated (z=0.92), creating a high-breadth exhaustion profile. (1)

- Momentum is clearly deteriorating as the index moved from -0.35 to 0.47 in under three months. (1)

- Conditional Invalidation: Index value exceeding 1.0 (High Alert threshold) or falling below 0.0. (1)

- Recent history shows persistent directional movement toward the "Elevated" stress boundary over the last six weeks. (1)

Scenario Balance:

- Base Case dominant: Typical market functioning continues but faces increasing friction and mean-reversion pressure.

- Most plausible upside risk: Orderly unwinding of crowded longs leads to a volatility-dampened consolidation.

- Most plausible downside risk: High extreme breadth triggers a volatility cluster and forced cross-asset liquidations.

Time Horizon & Aggregation:

- Time Horizon: Tactical (weeks). The signal tracks weekly positioning shifts and tactical reversal pressures. (1)

- Aggregation Weight Hint: Medium. The rising breadth of extremes warrants caution in risk-sensitive aggregations.

Macro Relevance:

- Informs the Systemic Liquidity and Positioning Risk dimension of the macro landscape. (1)

- The economic mechanism is positioning-led fragility; extreme crowding increases the probability of non-linear responses to data surprises. (1)

- Cycle position: Not determined.

- Typically acts as a lead indicator for volatility spikes and trend reversals in major asset classes. (1)

Regime Context:

- The current "Normal" regime has persisted for over 15 weeks but is currently strengthening toward the "Elevated" boundary. (1)

- Direction of change: Strengthening (increasing systemic positioning stress).

Model Limitations:

- Positioning extremes can persist in strong trends longer than standard statistical measures might suggest. (1)

- Commitment of Traders (CoT) data is subject to reporting lags which may mask real-time shifts. (1)

Data & References:

Early Warning System Chart

Portfolio-level stress indicators: extremes, crowding, squeeze/exhaustion, composite index.

Early Warning System Table▸

The information presented is for general informational purposes only and does not constitute financial or investment advice. It has been prepared without regard to individual objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek independent advice where necessary.