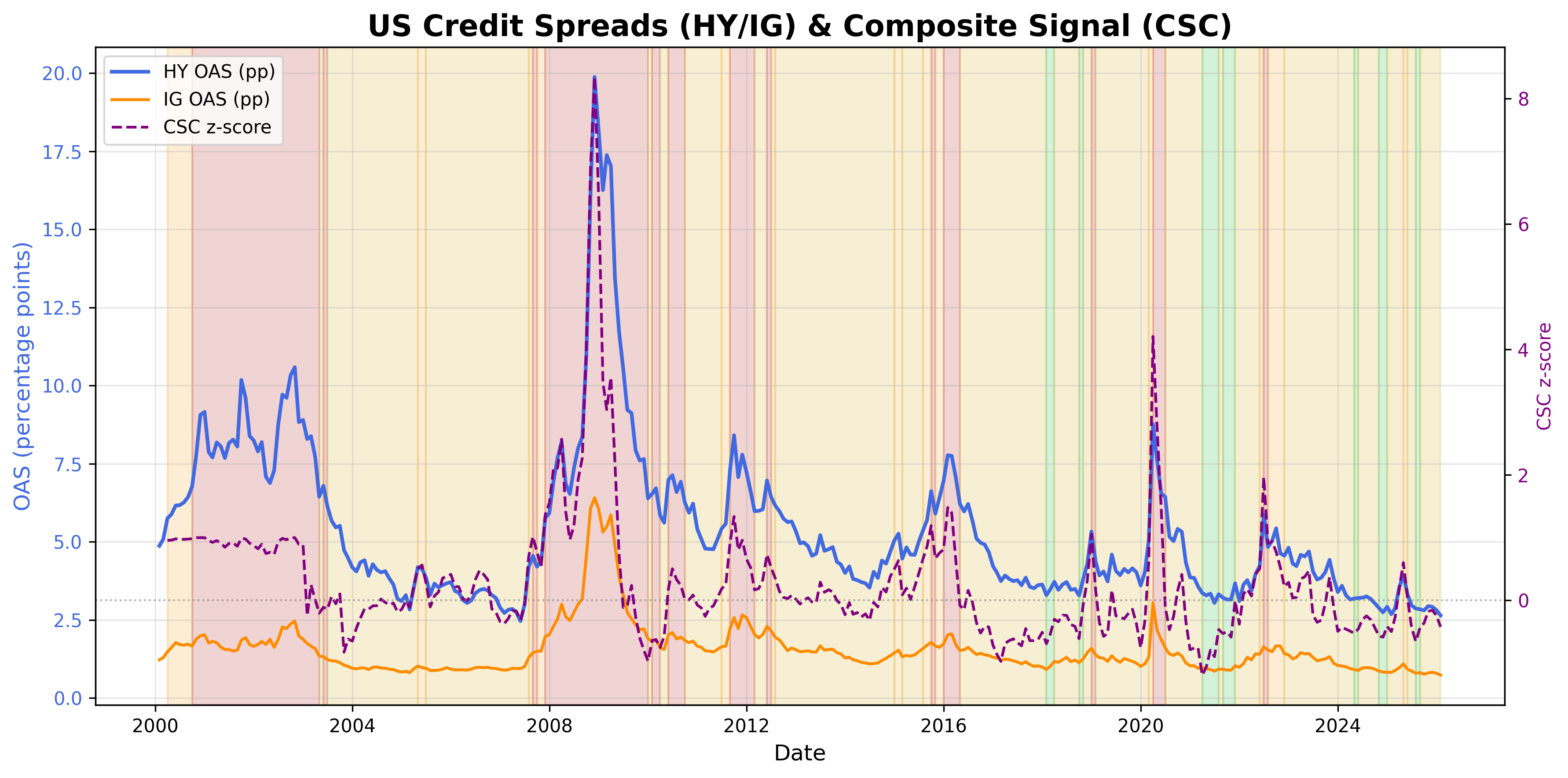

Credit Spreads Signal

Corporate credit spreads as a funding-stress and risk appetite indicator.

Gemini Summary

Signal Summary:

- Configuration statement: Given a HY_OAS of 3.27, a CSC_z of 0.08, and accelerating 3-month momentum (1.27), this setup aligns with Range-biased price paths and Normal volatility, where the dominant risk is Mean reversion, not Regime shift (1).

- The signal is currently in a NORMAL regime, reflecting credit conditions aligned with historical averages (1).

- Conviction Band: Medium; Interpretation Confidence: High Confidence; Internal Conflict Flag: No. Signal Stability Assessment: Deteriorating; Threshold Proximity: Near; Revision Sensitivity: Unknown.

Methodology Applied:

- A NORMAL regime is defined by High Yield (HY) spreads between 3.5% and 5% or a CSC z-score between -0.5 and 0.5 (1).

- The TIGHTENING regime is triggered if HY spreads rise >50bps in 3 months or the CSC z-score reaches ≥0.5 (1).

- Rising values imply a risk-off transition, tightening financial conditions, and an economic slowdown (1).

- Credit Spreads Signal, latest observation: 2026-03-31 (1).

Key Dynamics:

- The primary driver is the 3-month annualized momentum in HY spreads (z-score 1.27), indicating rapid widening from recent lows (1).

- Momentum has shifted from negative in early 2025 to consistently positive over the last quarter (1).

- Internal Tension: While HY spreads are widening, Investment Grade (IG) spreads remain more suppressed (z-score -0.55), suggesting stress is currently concentrated in lower-tier credit (1).

- Conditional Invalidation: An HY spread increase exceeding 50bps over 3 months would force a transition to a Tightening regime (current 3m change is +46bps) (1).

Scenario Balance:

- Base Case dominant: Continued range-bound Normal regime as spreads mean-revert toward historical averages.

- Upside risk: Transition to EASY regime if HY spreads fall below 3.5% and CSC_z drops below -0.5.

- Downside risk: Shift to TIGHTENING if current widening momentum persists, breaching the 50bps 3-month threshold.

Time Horizon & Aggregation:

- Time Horizon: Cyclical (months); captures shifts in default expectations and liquidity premia.

- Aggregation Weight Hint: Medium; provides a critical check on equity risk appetite and funding availability.

Macro Relevance:

- This signal informs the US Credit Conditions macro dimension by measuring the cost of corporate borrowing relative to risk-free rates (1).

- The economic mechanism is liquidity premia and default risk; rising spreads signal increased funding costs for cyclical firms (1).

- Cycle position: Not determined.

- Interaction: Typically confirms VIX movements; widening spreads with a calm VIX would signal credit-specific deterioration (1).

Regime Context:

- The NORMAL regime has been persistent for five consecutive months following a brief EASY phase (1).

- Direction of change: Strengthening/Deteriorating (spreads are moving from the bottom of the "Normal" range toward the "Tightening" threshold).

Model Limitations:

- Suffers from a 1-2 business day reporting lag and frequent vendor revisions (1).

- Bid-ask spread widening during market shocks can artificially inflate levels, creating microstructure noise (1).

Data & References:

Credit Spreads Chart

U.S. corporate credit spread dynamics.

Credit Spreads Table▸

The information presented is for general informational purposes only and does not constitute financial or investment advice. It has been prepared without regard to individual objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek independent advice where necessary.