U.S. Treasury Yield Curve Signal

U.S. Treasury curve shape as an indicator of growth and policy stance.

Gemini Summary

Signal Summary:

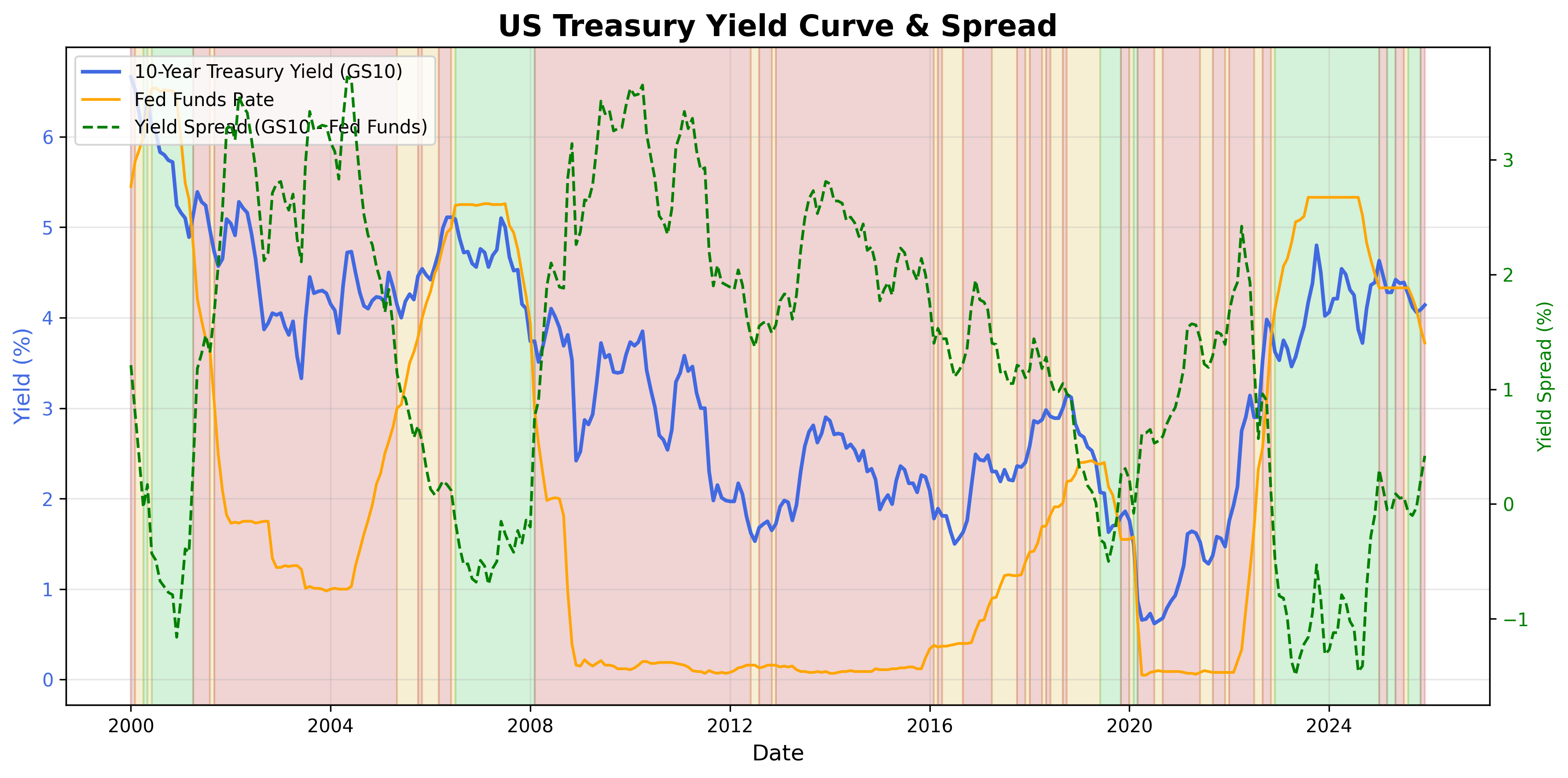

- Configuration statement (mandatory): Given a Yield_Spread of 0.49 and a GS10 rate of 4.13, this setup aligns with Range-biased price paths and Normal volatility, where the dominant risk is Mean reversion, not Trend continuation.

- The signal has transitioned from a three-month Bearish steepening phase into a Neutral regime as the spread stabilised below its three-month trend (1).

- Conviction Band: Medium, Interpretation Confidence: High Confidence, and Internal Conflict Flag: No. Signal Stability Assessment: Improving, Threshold Proximity: Near, and Revision Sensitivity: Moderate (1).

Methodology Applied:

- Yield Spread <= 0%: Economic curve inversion indicating restrictive monetary policy relative to growth expectations (1).

- 0% < Yield Spread <= 0.5%: Classification of a benign macro environment and stable term structure (1).

- Yield Spread > 3-month Trend: Identification of aggressive steepening associated with regime shifts (1).

- U.S. Treasury Yield Curve Signal dataset, latest observation: 2026-02-01 (1).

Key Dynamics:

- The primary driver is a Yield_Spread of 0.49, which falls within the 0% to 0.5% Neutral threshold (1).

- Momentum has slowed as the spread (0.49) converged with the 3-month trend (0.493), halting the recent steepening impulse (1).

- Conditional Invalidation: A move in the Yield_Spread below 0%, signalling renewed curve inversion and restrictive conditions (1).

- The signal shows improving stability after exiting a volatile steepening phase observed in late 2025 (1).

Scenario Balance:

- Base case dominant: Continued benign macro environment supported by a stable, non-inverted term structure (1).

- Upside risk: Bull-steepening expansion triggered by the spread exceeding the 3-month trend and 1.5% threshold (1).

- Downside risk: Transition to recessionary risk-off triggered by a return to negative yield spreads (1).

Time Horizon & Aggregation:

- Cyclical (months): Methodology defines this signal as a macro overlay with a 6–18 month lead time (1).

- Aggregation Weight Hint: Medium; the signal provides a high-level regime anchor but is not a tactical trigger (1).

Macro Relevance:

- Informs the pricing of duration risk and the balance between growth expectations and policy tightness (1).

- Economic mechanism: Measures the spread between long-term expectations and current monetary policy restrictiveness (1).

- Cycle position: Not determined.

- Typically interacts with real yields and credit spreads to validate systemic funding conditions (1).

Regime Context:

- The current Neutral regime is newly entered as of Feb 2026, following a persistent Bearish phase (1).

- Direction of change: Stabilising, as the spread recentres around its medium-term trend (1).

Model Limitations:

- Signal exhibits lagging behaviour (6–18 months) and conflates policy expectations with term premia (1).

Data & References:

- Latest observation: 2026-02-01. Influential datapoints: GS10 (4.13) and FEDFUNDS (3.64) (1).

- Public datasets like the VIX or High Yield Credit Spreads would improve interpretation of systemic stress levels.

U.S. Treasury Yield Curve Chart

Treasury yield curve across maturities.

Treasury Yield Curve Table▸

The information presented is for general informational purposes only and does not constitute financial or investment advice. It has been prepared without regard to individual objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek independent advice where necessary.