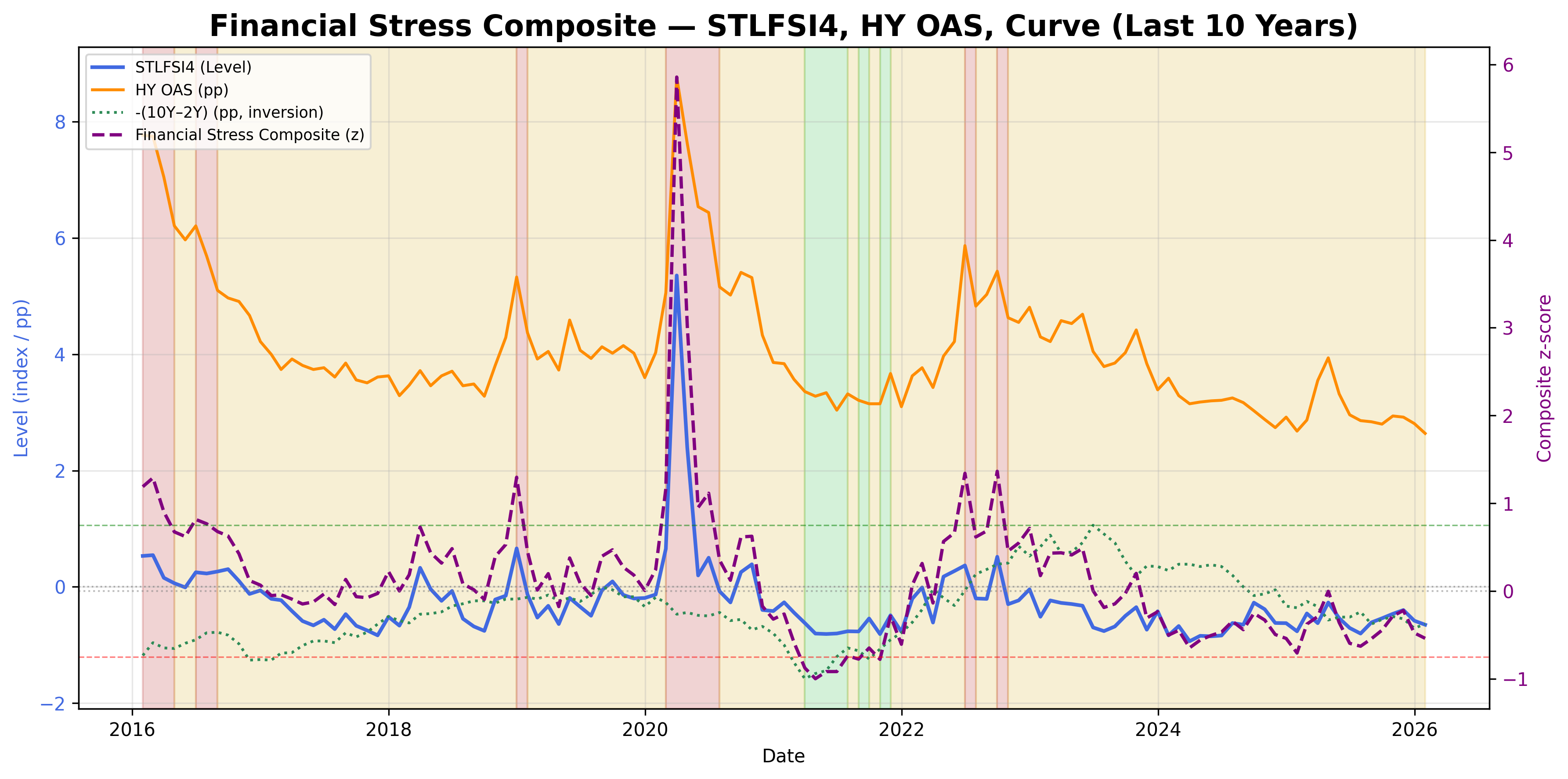

Financial Stress Composite Signal

Systemic stress from credit spreads, curve inversion, and financial conditions.

Gemini Summary

Signal Summary:

- Configuration statement: Given a Fin_Stress reading of 0.045, an STLFSI4 z-score of 0.677, and a T10Y2Y z-score of -0.489, this setup aligns with Range-biased price paths and Normal volatility, where the dominant risk is Mean reversion, not Regime shift. (1)

- The signal currently occupies a Neutral regime, reflecting financial conditions that align with historical norms. (1)

- Conviction Band: Medium; Interpretation Confidence: High Confidence; Internal Conflict Flag: No. Signal Stability Assessment: Volatile; Threshold Proximity: Far; Revision Sensitivity: Unknown.

Methodology Applied:

- Composite readings between -0.75 and 0.75 define the Neutral regime, implying market stability and historical alignment. (1)

- Readings above 0.75 signify High Stress and risk-off conditions, while those below -0.75 indicate Low Stress and risk-on expansion. (1)

- The signal weights funding liquidity (STLFSI4), corporate default risk (HY_OAS), and policy expectations (T10Y2Y). (1)

- Financial Stress Composite Signal: Latest observation 2026-03-31. (1)

Key Dynamics:

- The primary driver is a sharp rise in the STLFSI4 z-score (from -0.31 to 0.67 in two months), indicating increasing broad market volatility. (1)

- This pressure is offset by the corporate credit component (HY_OAS z-score of -0.05), which suggests default risk remains contained. (1)

- The Yield Curve (T10Y2Y) is moving deeper into negative z-score territory (-0.489), reflecting a move away from policy-led stress (inversion). (1)

- Conditional Invalidation: A move in the Composite index above 0.75. (1)

- Stability is currently low as the signal has transitioned from a deeply accommodative stance (-0.52) toward the zero-line. (1)

Scenario Balance:

- Base Case dominant: Continued range-bound stability as credit spreads and liquidity volatility provide opposing forces.

- Upside risk: Transition to Low Stress triggered by a reversal in broad market volatility (STLFSI4).

- Downside risk: Transition to High Stress triggered by a sudden widening of corporate credit spreads (HY_OAS).

Time Horizon & Aggregation:

- Time Horizon: Cyclical (months) as the composite filters high-frequency noise to identify durable shifts in funding conditions.

- Aggregation Weight Hint: Medium; while the signal is fresh, its proximity to zero suggests it acts as a neutral anchor rather than a directional catalyst.

Macro Relevance:

- Informs the liquidity and credit dimensions by measuring the intersection of volatility and risk premia. (1)

- The economic mechanism implied is a tension between rising market uncertainty and resilient corporate funding access. (1)

- Cycle position: Not determined.

- Typically serves as a confirmation tool for risk-appetite signals like credit spreads and the VIX. (1)

Regime Context:

- The Neutral regime is highly persistent, having remained in place throughout the provided history since April 2023. (1)

- Recent direction of change is strengthening (moving from the lower/accommodative end of Neutral toward the center). (1)

Model Limitations:

- Monthly frequency may miss intra-month liquidity spikes. (1)

- Potential double-counting exists between STLFSI4 and High Yield OAS components. (1)

Data & References:

Financial Stress Composite Chart

Composite of STLFSI, HY spreads, and yield-curve inversion.

Financial Stress Composite Table▸

The information presented is for general informational purposes only and does not constitute financial or investment advice. It has been prepared without regard to individual objectives, financial situation, or needs. You should consider whether it is appropriate for your circumstances and seek independent advice where necessary.