Silver Price Research

Institution-level institutional silver target extraction from IA researcher PDFs, with historical target tracking and synthesis.

Market Interpretation

Current Median Target

85.00

Recent (latest 90 days)

Current Target Range

84.50 - 222.00

Focus window min/max

Recent Forecast Count

7

Numeric rows driving current view

Median Shift vs Prior

↑ +7.50

Prior median: 77.50

Latest Publication

2026-05-01

Based on publication dates in the latest 90 days.

Comparability

Moderate

Recent window mixes direct and derived targets.

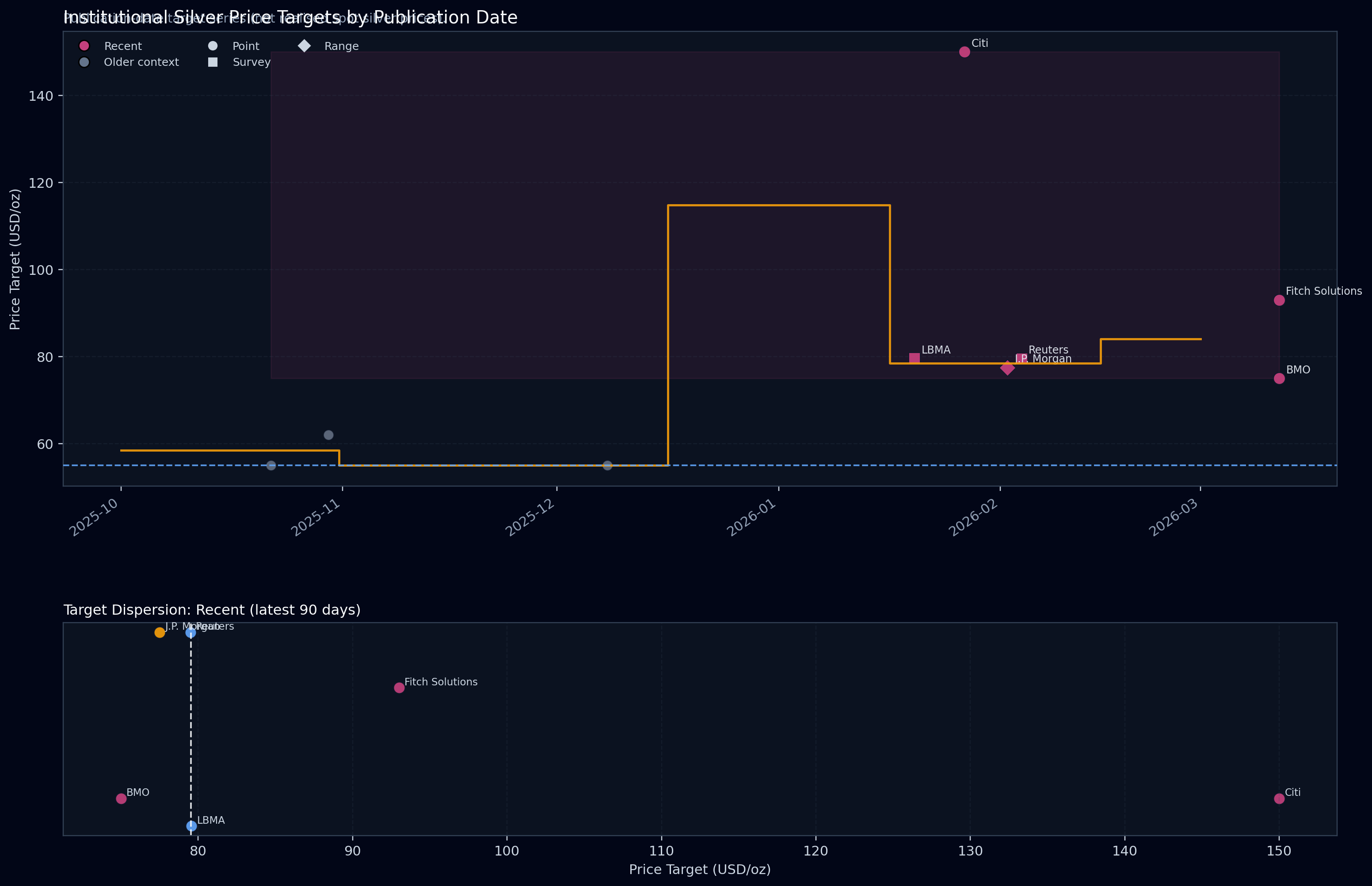

Current View: The institutional outlook for silver has shifted significantly higher over the first half of 2026, with the most recent forecasts now centering on a median of $85.00 per ounce. This represents a distinct upward move from the prior median of $77.50, reflecting a broad trend of upward revisions across major financial institutions. While the distribution of targets has clearly moved higher, the consensus appears to be consolidating around this new elevated baseline as the market digests the aggressive price action seen earlier in the year.

Recent Revisions: Within the latest 90-day focus window, institutional forecasts show a tightening cluster between $80 and $95 for 2026 averages. For example, UBS recently adjusted its mid-2026 target to $85.00 from a previous $100.00 expectation, citing revisions to mine supply expectations while maintaining a bullish fundamental stance. Similarly, ING and Fitch Solutions have positioned their 2026 averages at $83.00 and $93.00 respectively, indicating that the core institutional expectation has moved decisively away from the mid-$70s consensus observed earlier in the year.

Outlook Dispersion: The current target distribution is marked by significant upside dispersion, particularly regarding tactical bull cases versus base-case averages. Bank of America has modeled extreme scenarios ranging from $135 to $309 per ounce based on potential gold-to-silver ratio compression, while simultaneously noting a more conservative peer consensus cluster between $79 and $90. This wide spread between standard point forecasts and tactical "tail-risk" projections suggests that while conviction in the upward trend remains high, there is considerable uncertainty regarding the potential for parabolic price peaks.

Historical Context: Current price targets represent a substantial reappraisal compared to late 2025, when the institutional outlook was significantly more tempered. During the final quarter of 2025, major banks such as BMO, HSBC, and Bank of America were projecting 2026 averages in the $45 to $65 range. The fact that recent "softened" targets like the $85.00 level from UBS are still nearly double the year-ago expectations highlights a massive upward shift in the perceived floor for the silver market.

Key Drivers: The primary catalyst for this upward shift is the expectation of a sixth consecutive annual market deficit. Analysts across the dataset consistently point to inelastic supply—largely a result of silver’s status as a mining by-product—meeting surging industrial demand from the solar, electric vehicle, and AI infrastructure sectors. Additionally, silver’s high beta relative to gold and its role as a hedge against currency debasement remain central themes in the current high-conviction pricing models.

Comparability and Data Limitations: It is important to note that the comparability of these targets is limited by differing methodologies and horizons. The dataset blends annual averages, quarterly point targets, and news poll medians, which do not always align in timeframe. Furthermore, several key industry bodies like the Silver Institute and World Gold Council provide the fundamental supply-demand data that underpins these forecasts but do not publish numeric price targets themselves, leaving the quantitative outlook dependent on the varying models of investment banks and research houses.

Target Visuals

Recent forecasts are emphasised; older retained forecasts provide historical context. Targets represent extracted institutional expectations, not realised silver prices.

Extracted Data (Validation)▸

All views expressed are personal, based on publicly available information, and do not represent the views of any employer or reflect any proprietary or internal analysis. This information should not be relied upon for making investment decisions.

No representation or warranty is made as to the accuracy, completeness, or timeliness of the information, and no liability is accepted for any loss arising directly or indirectly from its use.