Investor Anatomy Series

A structured, signal-driven synthesis of the silver market, integrating macro drivers, price behaviour, and institutional research into a single, decision-grade view.

Silver Outlook Podcast

Silver remains underpinned by a robust liquidity expansion regime and a weakening US dollar, though the market faces immediate constraints from fragile speculative positioning and a disconnect between macro tailwinds and recent price action.

Executive Summary

The silver market, currently priced near 63.39 in the iShares Silver Trust, is operating under the dominant force of global liquidity expansion. While the underlying macro environment is supportive, we maintain a neutral to mixed directional bias in the near term as the market digests a recent period of speculative long reduction. The path forward remains contingent on whether the technical recovery can realign with these improving liquidity conditions.

Opening Thesis

We characterize the current silver system as conflicted, moving through a transition where fundamental supports are at odds with market expression. While expansionary liquidity and dollar weakness provide a clear tailwind, price action has lagged, creating a distinct macro-price disconnect. The dominant force at play is the easing of financial conditions, yet this is currently being masked by a tactical retreat in speculative conviction. This setup suggests that while the floor for the metal is rising, the momentum required for a sustained breakout is still forming.

Outlook

Over a one-month horizon, if the recent geopolitical de-escalation continues to lower energy-driven inflation expectations, we expect silver to undergo a period of tactical consolidation as it attempts to recapture its shorter-term moving averages. Looking out three months, if the expansionary liquidity regime persists and the US dollar continues its weakening trend, the bias shifts to bullish as silver typically exhibits high beta performance in such environments. On a twelve-month strategic basis, if the projected sixth consecutive annual market deficit remains the primary fundamental anchor and real rates stay in their current neutral band, we anticipate price levels will gravitate toward the newly elevated institutional median targets.

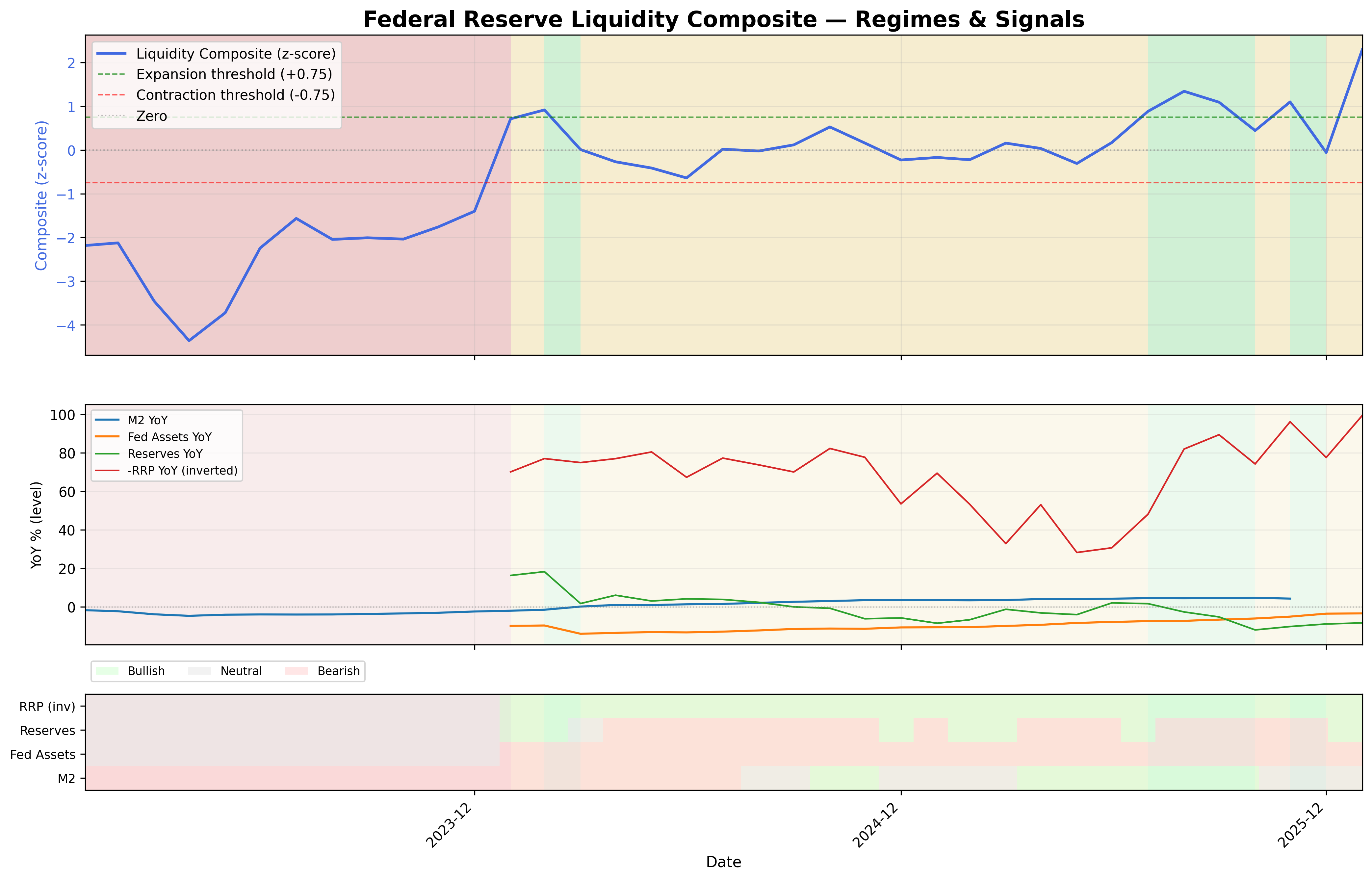

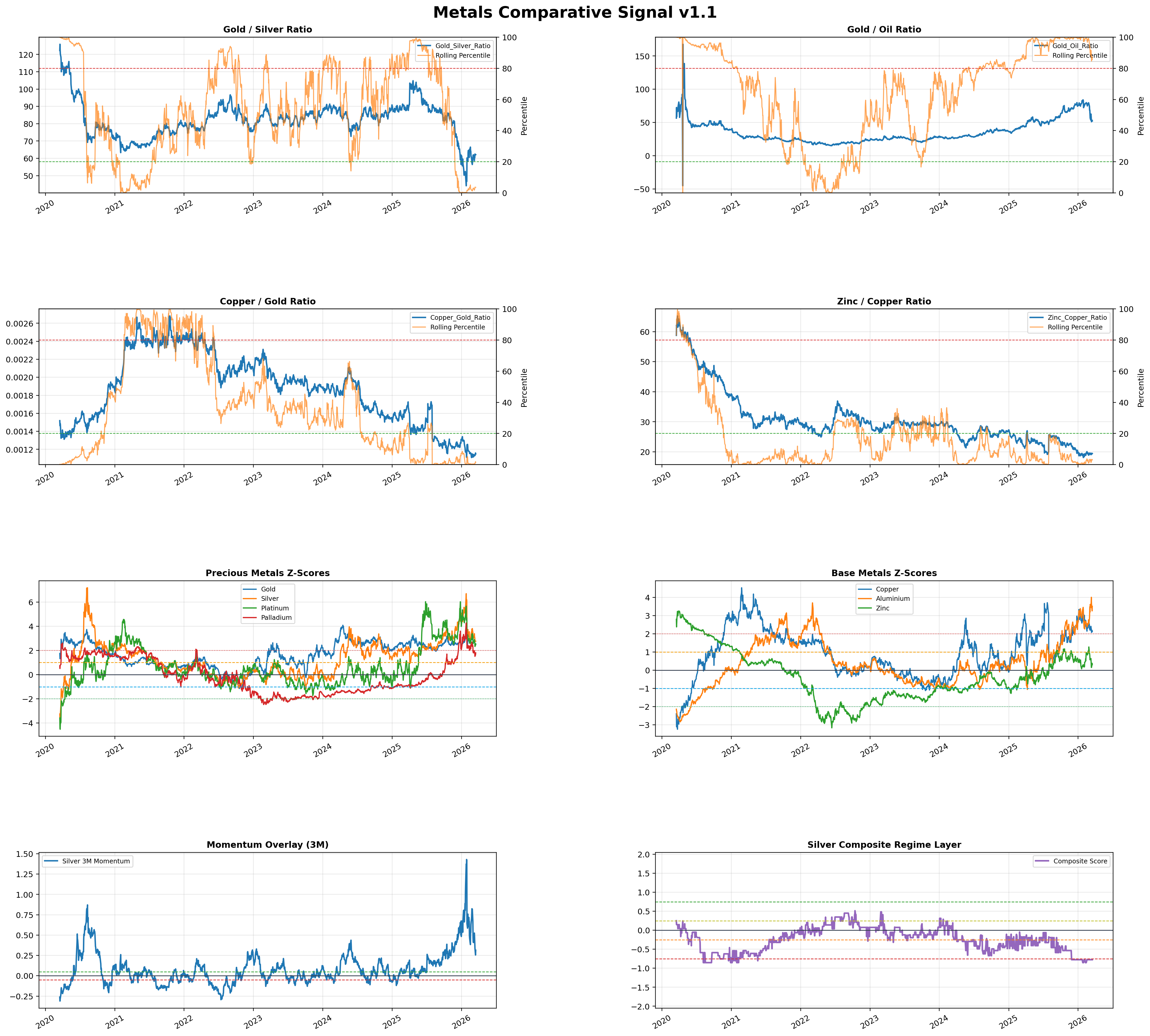

Market Regime and Macro Drivers

The silver market is firmly situated within a liquidity expansion regime, which serves as the primary driver of value in the current environment. This expansionary backdrop is reinforced by a weakening US dollar, a combination that historically provides the most fertile ground for precious metals appreciation. These forces are currently overriding a neutral real rate environment and contained inflation signals, suggesting that the primary causality for price movement is now rooted in capital availability rather than immediate inflationary hedging. We define the overall regime condition as supported but fragile, as the tailwinds of the liquidity composite must now contend with a transition in central bank leadership and shifting monetary expectations.

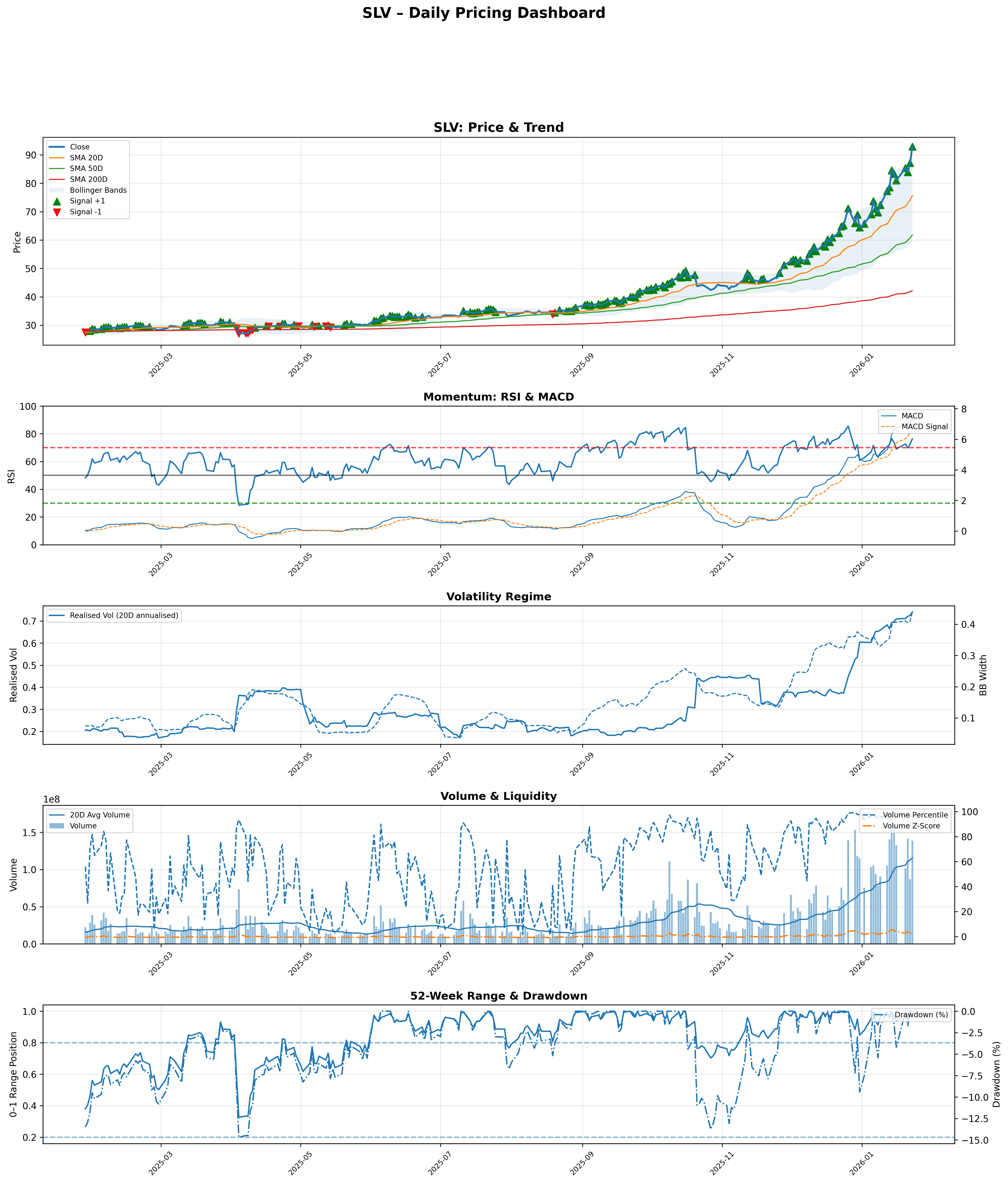

Price Action

Anchoring our analysis to price reality, the iShares Silver Trust closed recently at 63.39, placing it firmly in the middle of its 52-week range. This follows a period of significant volatility where the asset fell below its 50-day moving average of 68.25 but found reliable support above the 200-day trend line of 61.52. We classify the current price regime as a consolidation phase following a failed breakout attempt. While the long-term trend remains intact, the failure to hold the 50-day average suggests that price is currently resisting the broader bullish macro regime, indicating a need for a period of base-building before the next move higher.

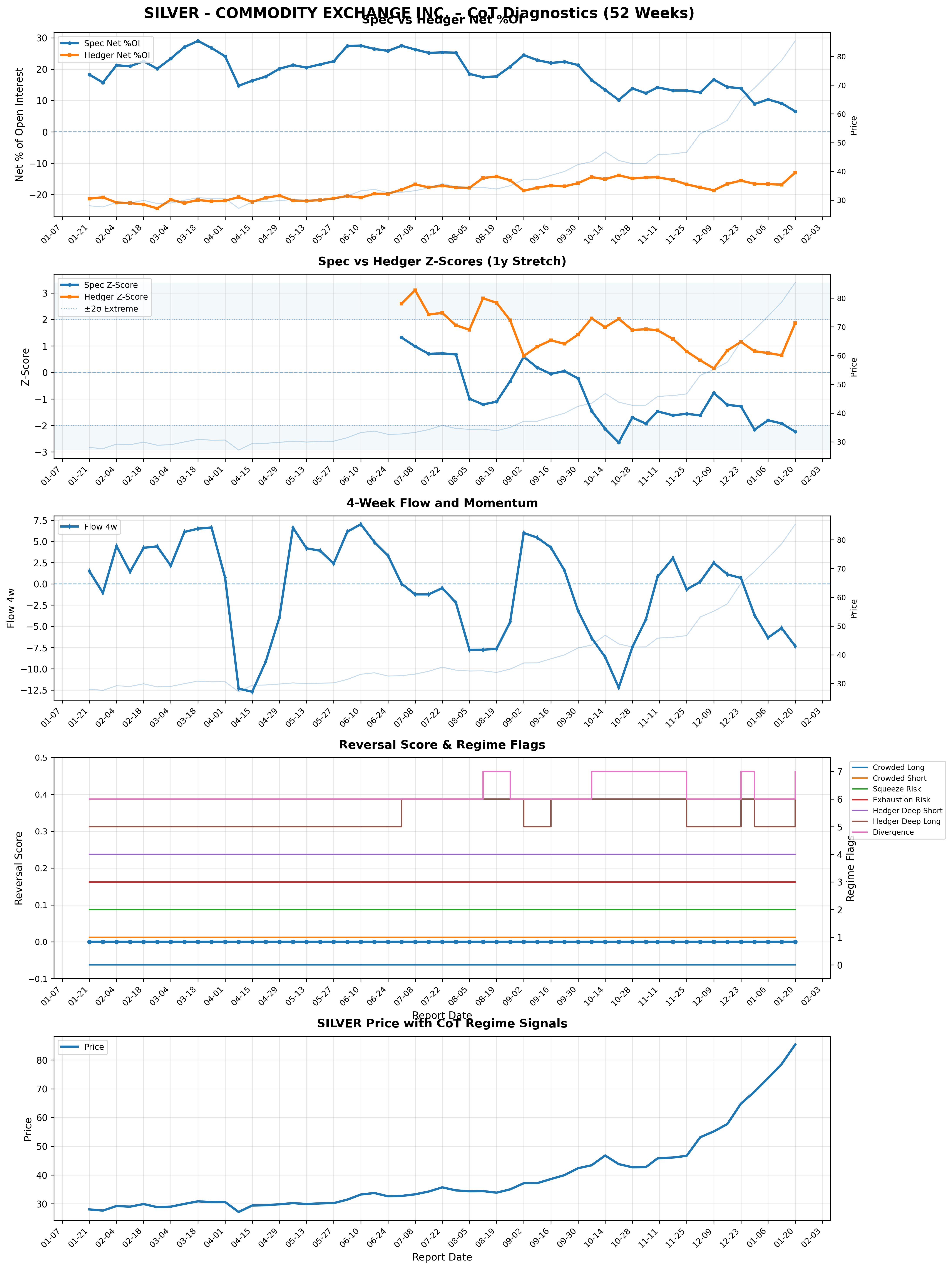

Market Expression and Capital Flows

Positioning data reveals a lack of conviction among active participants, with a significant negative four-week flow of -5.13. This indicates a long reduction phase where speculators are de-risking despite the supportive macro backdrop. ETF flows reinforce this cautious stance; the iShares Silver Trust saw a recent outflow of 1.2 million shares, though the overall flow regime remains classified as neutral. We conclude that capital is currently diverging from the macro regime, with professional positioning acting as a drag on price rather than a catalyst for expansion.

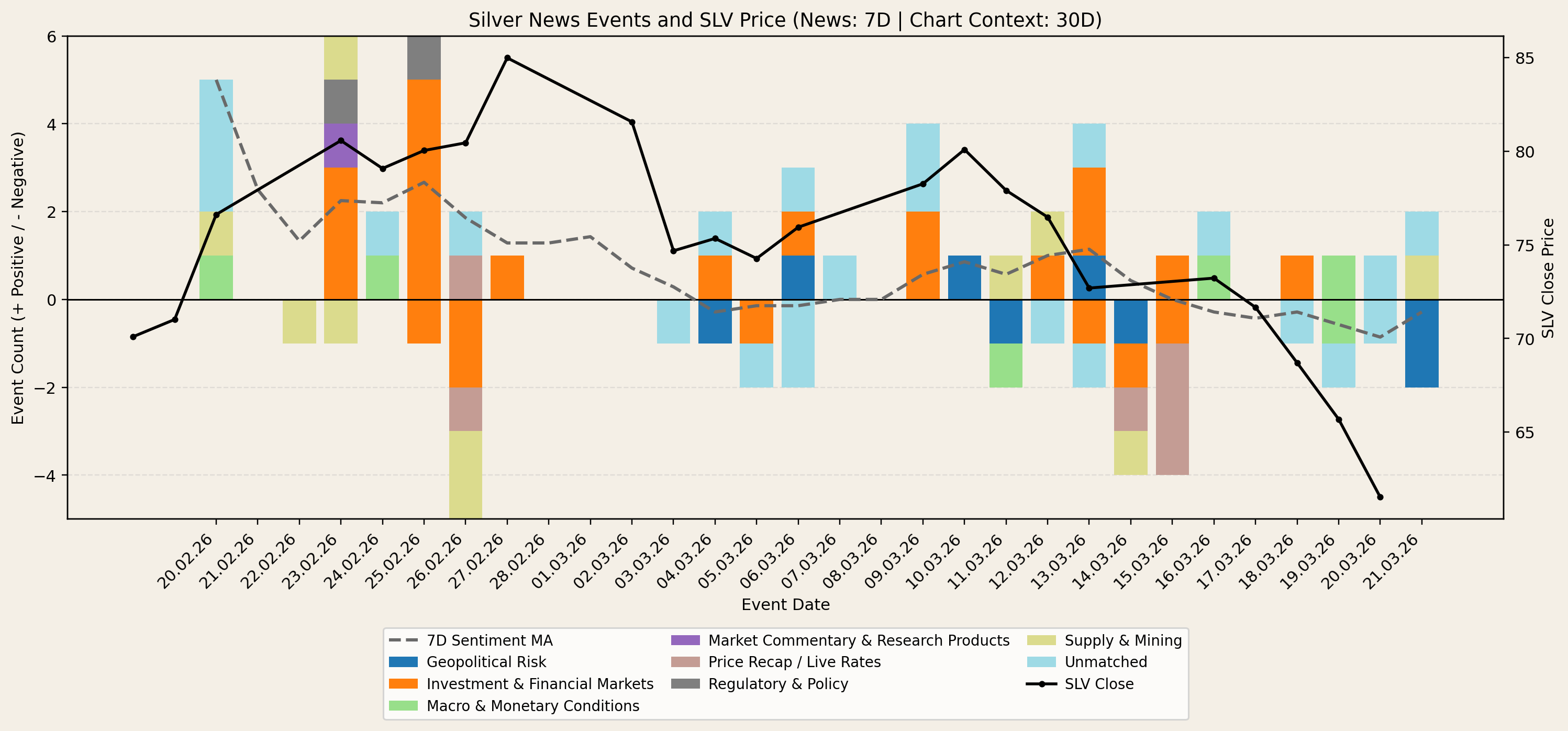

News Flow and Narrative

The dominant narrative has shifted toward a transition in monetary leadership and the potential for regional stability following geopolitical easing. The market is intensely focused on the Federal Reserve’s policy direction under new leadership and the impact of a potential ceasefire in the Middle East on energy costs and inflation expectations. Additionally, the narrative of a structural supply deficit continues to provide a long-term fundamental floor, even as short-term news flow remains volatile. We view the current narrative as reinforcing for the long term but transitional for the immediate future as the market awaits clarity on the next phase of US interest rate policy.

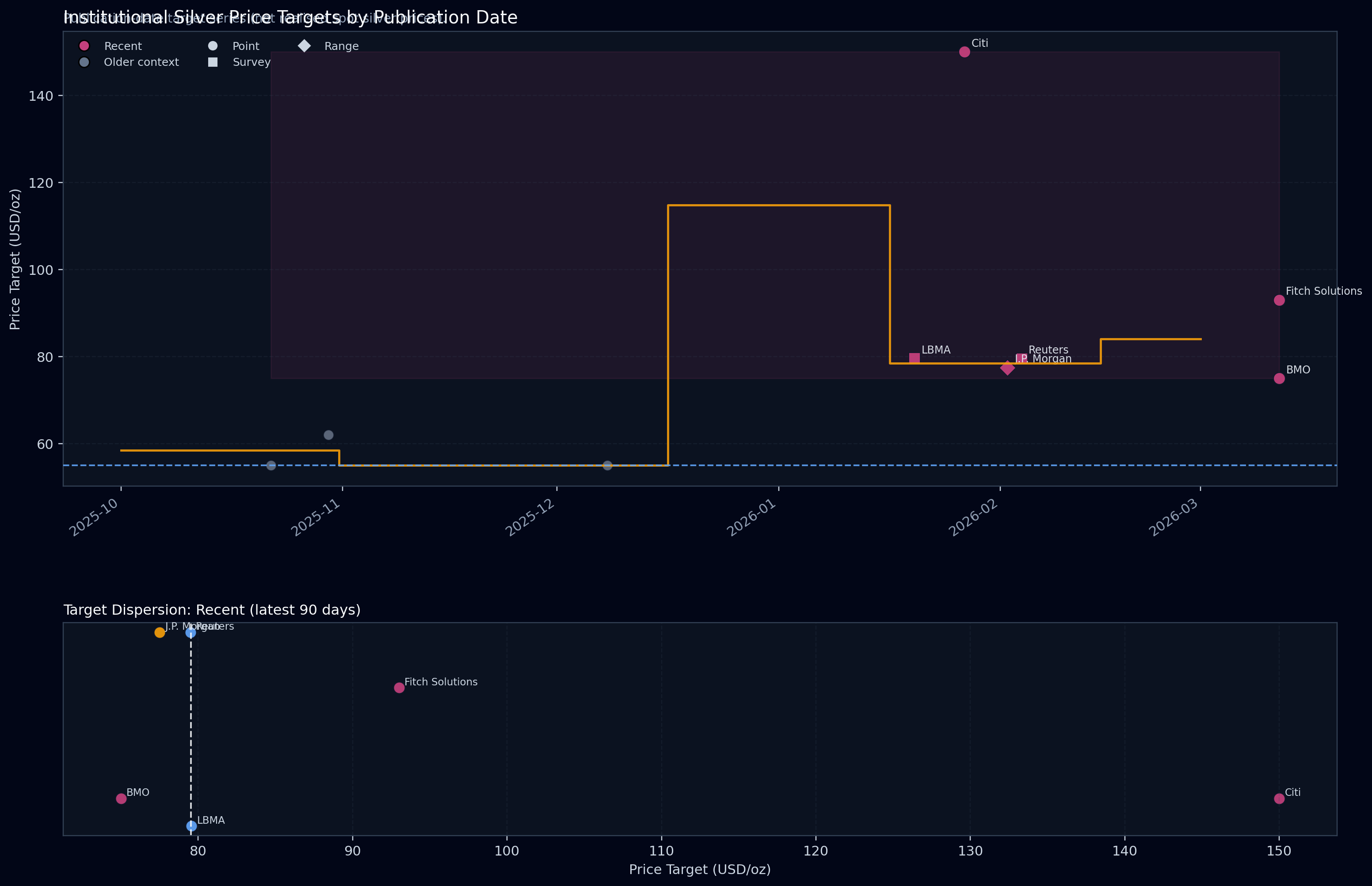

Target Pricing and Research

Institutional research has undergone a significant upward reappraisal, with the median target for silver now anchored at 85.00 per ounce, up from a previous baseline of 77.50. Our base case range for the next twelve months sits between 80.00 and 95.00, while aggressive upside scenarios modeled by some institutions reach as high as 222.00 in the event of a significant compression in the gold-to-silver ratio. The downside stress range is defined near 75.00, a level that would likely be tested only if the current liquidity expansion were to abruptly reverse. The primary driver of movement between these ranges remains the persistent physical deficit and surging industrial demand from the green energy and technology sectors.

Conflicts, Risks & Invalidation Watchpoints

The primary conflict in our system is the divergence between high-conviction macro signals and weakening market participation. This fragility is compounded by exhaustion signals in the broader industrial metals complex, with copper and aluminum reaching statistically stretched levels that may lead to a sympathy sell-off in silver. Our primary invalidation trigger is a transition of the US dollar from its current weakening state to one of dominant strength, or a spike in market volatility where the VIX breaches the 20 level. If either occurs, the liquidity tailwinds would be overridden, and the current bullish thesis would be structurally weakened.

Closing

In summary, while silver remains supported by a favorable liquidity expansion and a softening dollar, the market is currently constrained by a tactical retreat in investor positioning and industrial sector exhaustion. Our mental model views this as a market with a rising fundamental floor but a temporary ceiling defined by technical resistance and de-risking flows. The system remains aligned with long-term growth but is tactically fragile, requiring a reconnection between price action and its macro drivers to resume its upward trajectory.

All views expressed are personal, based on publicly available information, and do not represent the views of any employer or reflect any proprietary or internal analysis. This information should not be relied upon for making investment decisions.

No representation or warranty is made as to the accuracy, completeness, or timeliness of the information, and no liability is accepted for any loss arising directly or indirectly from its use.