Investor Anatomy Series

A structured, signal-driven synthesis of the lithium market, integrating macro drivers, price behaviour, and institutional research into a single, decision-grade view.

Lithium Outlook Podcast

The lithium market is transitioning out of a prolonged period of extreme speculative bearishness, driven by a structural shift toward balance-sheet resilience and international supply alliances, though current momentum remains constrained by a pause in retail capital inflows.

Executive Summary

The lithium market, proxied by the miners and producers ETF, is currently consolidating near 19.32 after a period of high realized volatility. The dominant force acting on the market is a positioning reversal as speculators exit extreme short configurations. We maintain a constructive near-term directional bias, conditional on the continued stabilization of global liquidity and the successful execution of recent supply chain agreements.

Opening Thesis

What we are observing now is a fundamental transition from a regime defined by crowded short-selling to one characterized by fragile balance. This shift matters because it suggests that the floor for lithium pricing is being reinforced by institutional de-risking rather than just temporary scarcity. The system is currently transitioning, with the dominant force being a speculative positioning reversal that is overriding lingering macroeconomic concerns. We see a market that is looking for a new equilibrium as the narrative pivots from raw price volatility to long-term industrial mineral security.

Outlook

Our outlook across three horizons is dictated by the interaction of positioning and liquidity. Over the one-month tactical horizon, if the current positive flow of speculative long building continues, we expect a constructive drift toward the upper end of the recent range. However, if this short-covering impulse fails to attract secondary retail sponsorship, the market will likely return to a range-bound state. Looking at the three-month cyclical view, if the broad expansion of money supply and the risk-on shift in financial stress persist, the system should find support for a sustained recovery. On a twelve-month strategic basis, if the anticipated demand for energy storage systems materializes and supply project delays continue, the price floor will likely reset to the twenty-thousand-dollar range defined by institutional research.

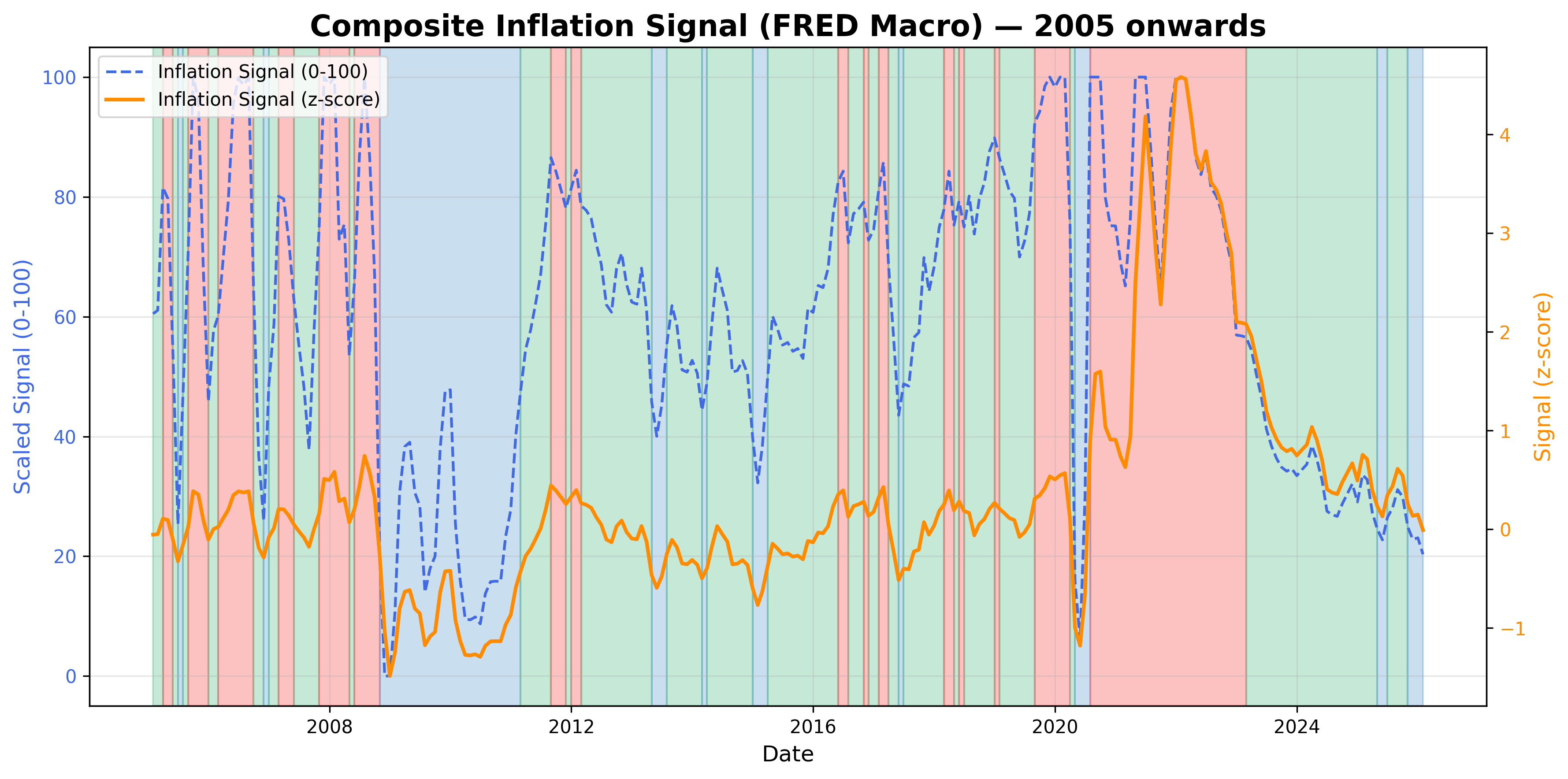

Market Regime and Macro Drivers

The dominant force currently shaping the macro regime is the expansion of global liquidity and a general shift toward a risk-on posture in financial conditions. These tailwinds are successfully overriding the constraints typically imposed by currency volatility and mixed signals from central banks. We identify the overall regime as a fragile balance, where the systematic reduction of debt by major producers and the formalization of international critical mineral alliances are providing a buffer against a cooling global economic outlook. This causal chain suggests that the lithium-specific supply-chain hardening is currently more influential than broader trade-sensitive currency dynamics.

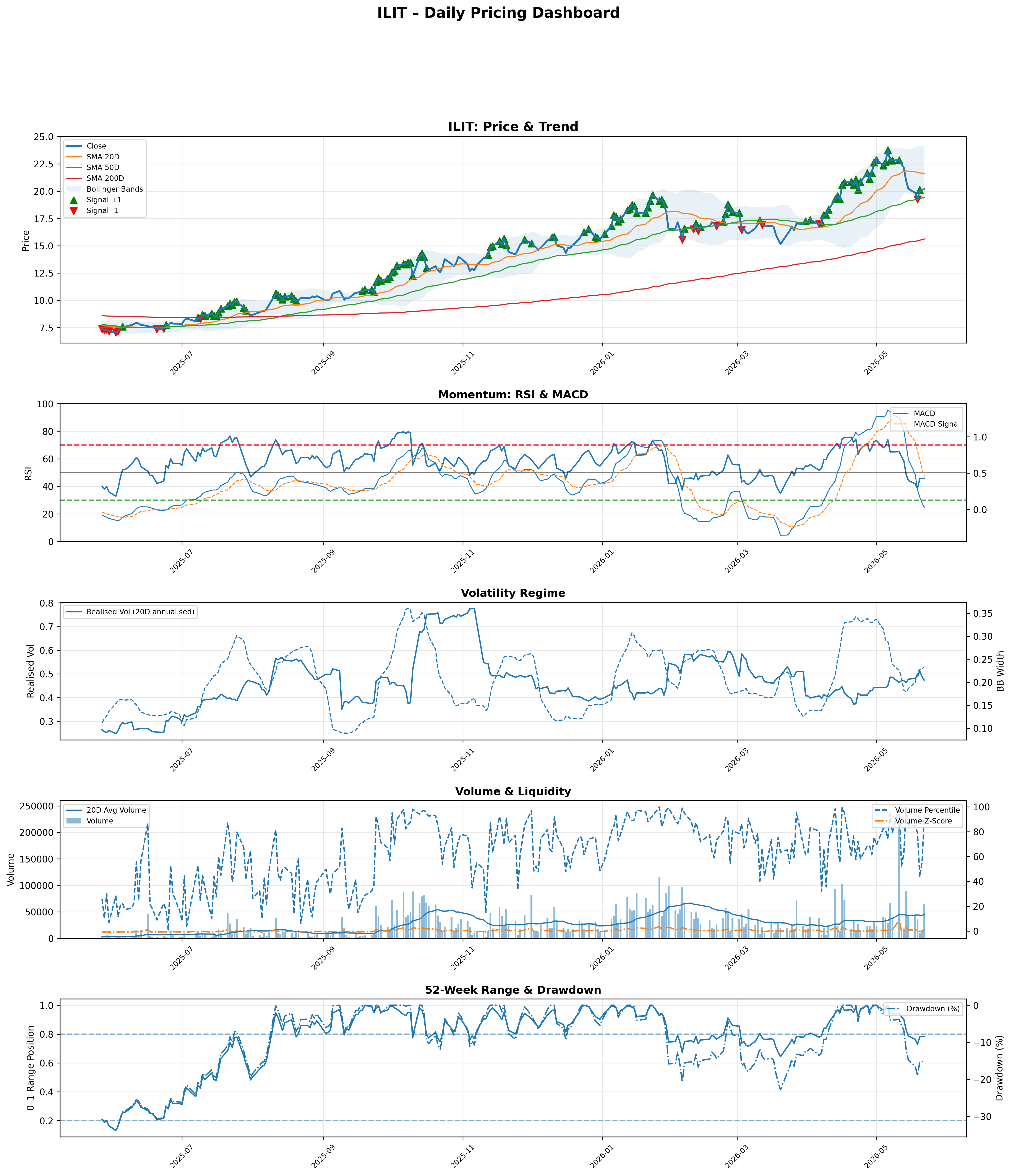

Price Action

Anchoring our analysis to price reality, the market is currently trading around the 19.32 level, representing a significant consolidation after a volatile drawdown earlier in the month. Price is presently situated between key technical reference levels, holding above the 200-day moving average but remaining below the 50-day trend line. We classify this price regime as bottoming, characterized by a mid-range position within the 52-week band. This behavior confirms our regime transition thesis, as the market resists further breakdown despite the absence of a decisive breakout attempt.

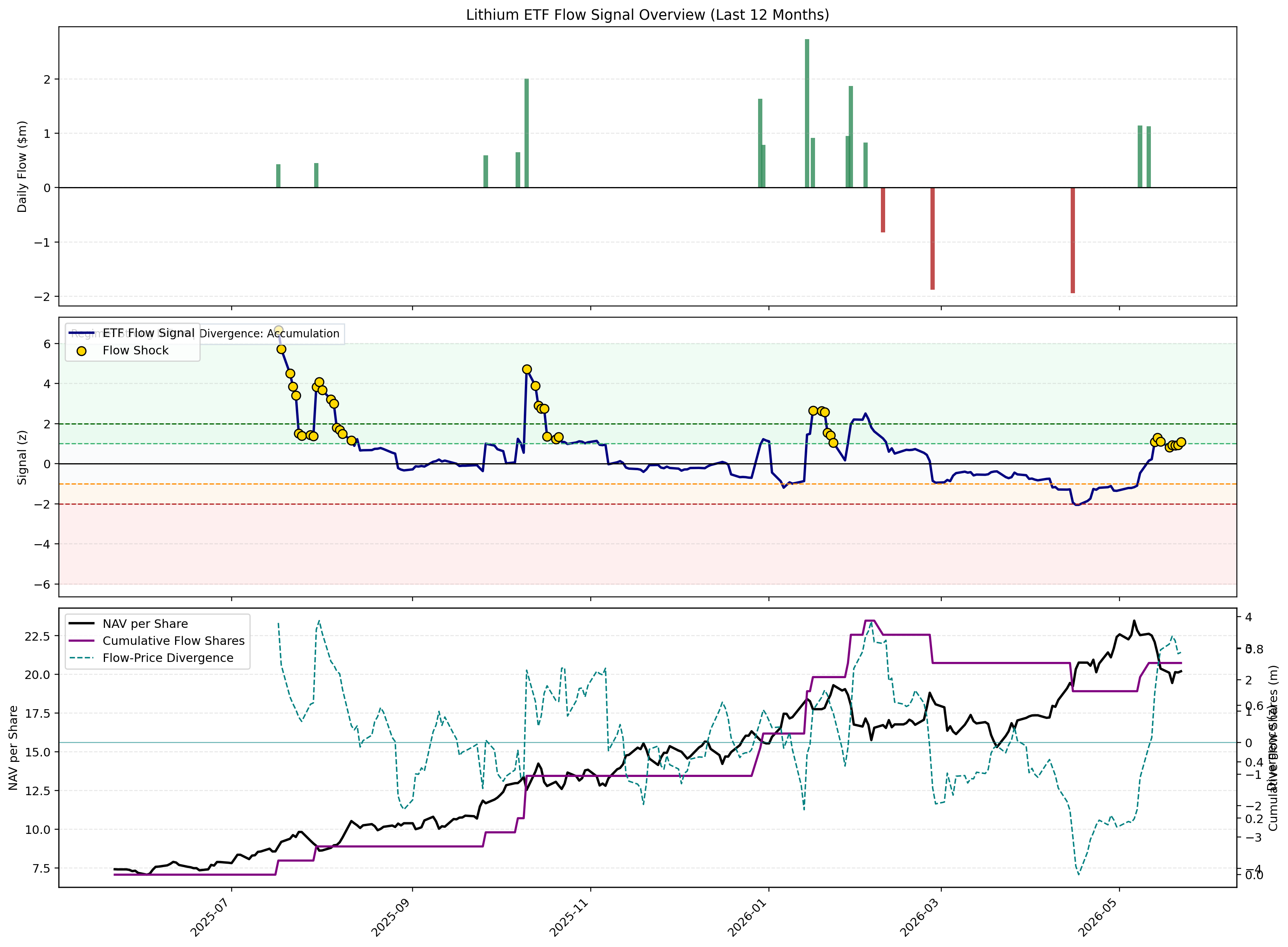

Market Expression and Capital Flows

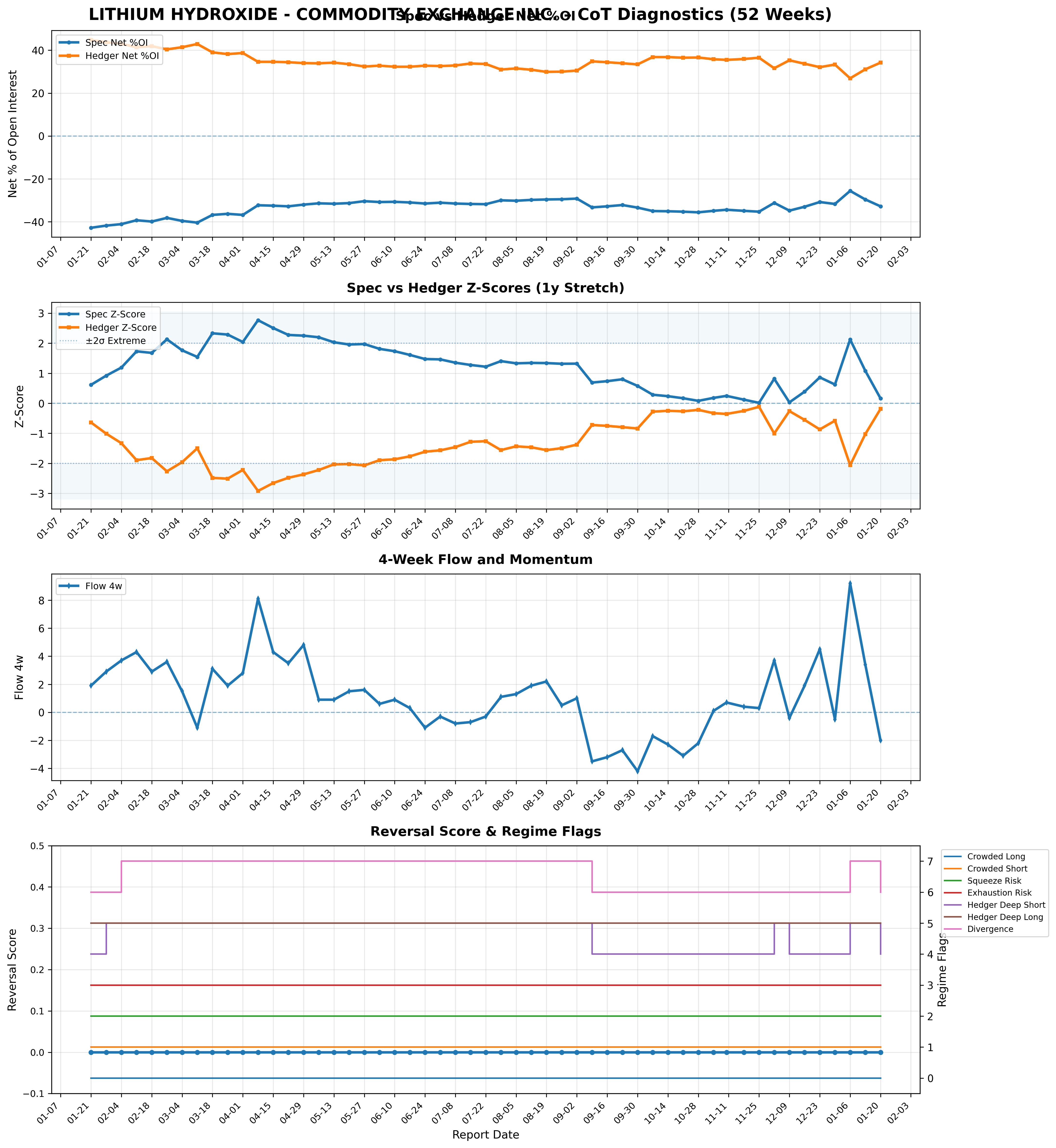

Recent flow data presents a study in divergence. While speculative positioning in lithium hydroxide futures has shown a positive four-week build, indicating a move away from extreme short crowding, retail and institutional interest via ETFs has entered a neutral regime. Share creation has effectively stalled since early June, with the 20-day flow momentum indicating a deceleration of liquidity support. We conclude that capital is currently neutral and slightly diverging from the bullish positioning reversal seen in derivative markets, suggesting that while the "sell" conviction has faded, the "buy" conviction has not yet reached extreme levels.

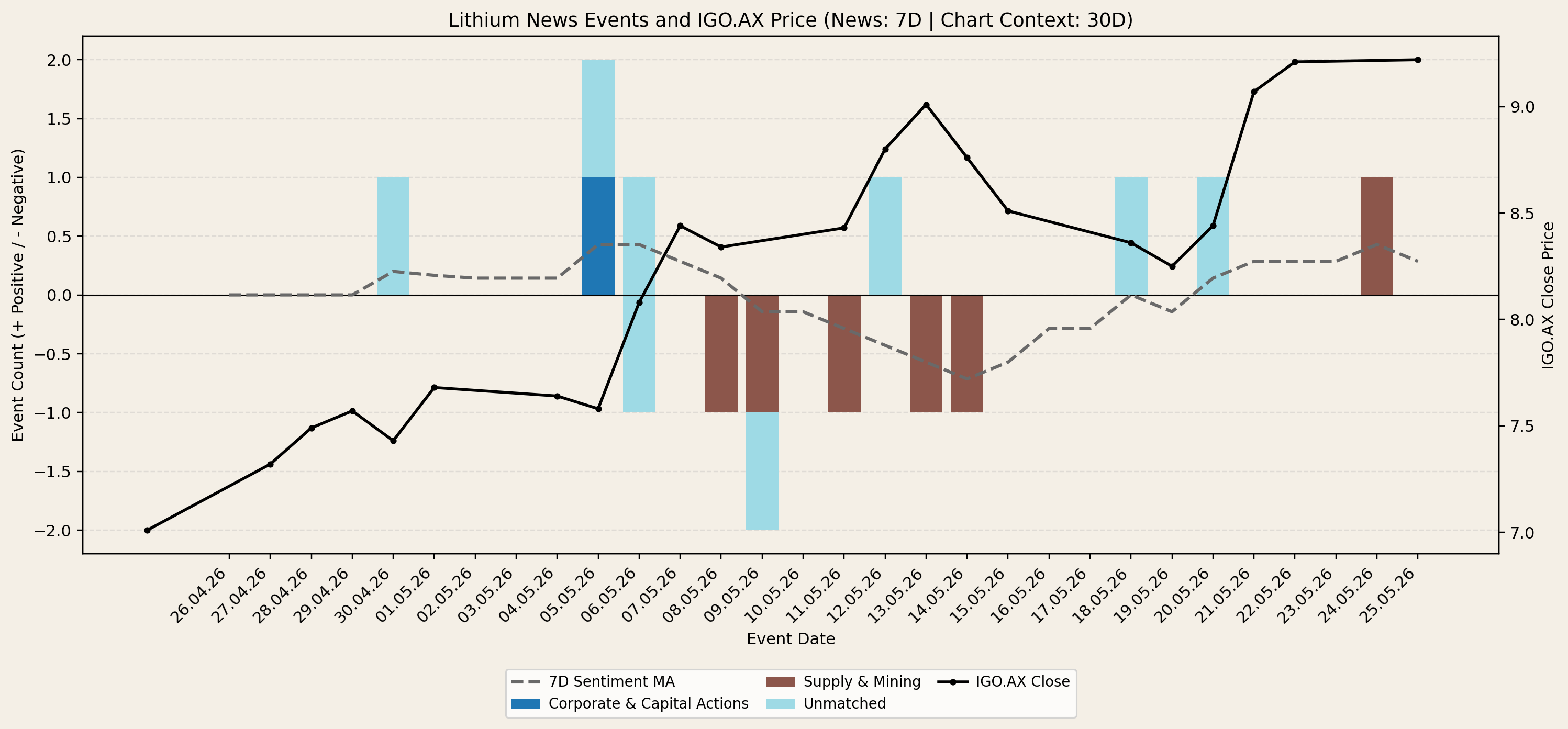

News Flow and Narrative

The narrative environment has shifted toward a more mature and supportive tone, dominated by two primary themes. First, we are seeing a "balance-sheet reset" among industry leaders who are aggressively deleveraging to manage interest costs. Second, the institutionalization of the lithium supply chain is intensifying through G7-led alliances and high-level offtake agreements. The market is increasingly focused on financial flexibility and strategic mineral security over short-term price speculation. We view this narrative as reinforcing the stabilization of the asset class, signaling that major players are preparing for a long-cycle recovery.

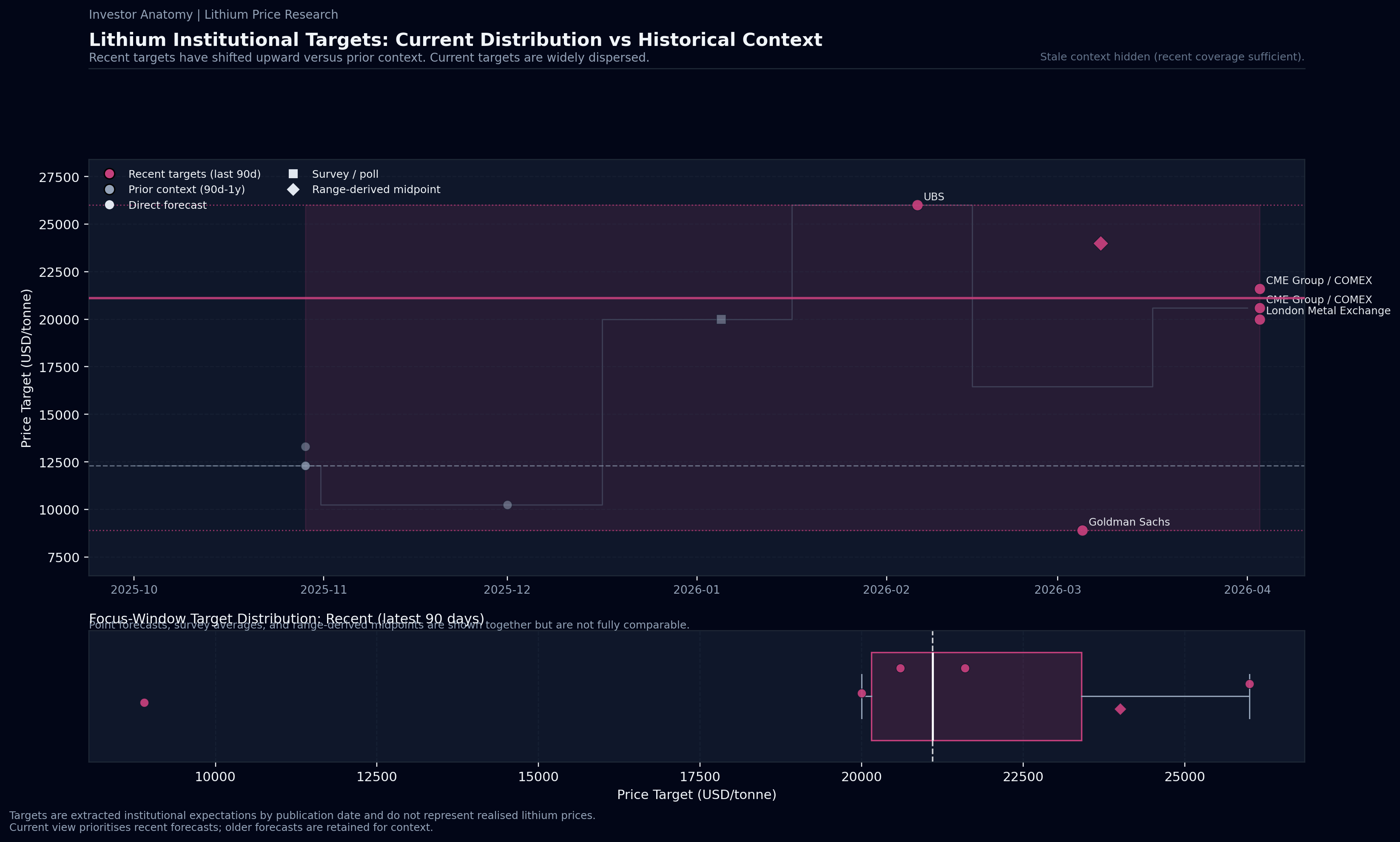

Target Pricing and Research

Institutional research now provides an anchor with a base case median target of approximately 20,600 dollars per tonne for lithium hydroxide. This represents a substantial upward shift from the targets seen in late 2025. The current upside scenario stretches toward 26,000 dollars, predicated on spodumene conversion constraints and electric vehicle demand uplift. Conversely, the stress range remains as low as 8,900 dollars in a scenario where a significant wave of new supply overwhelms the market. The movement between these ranges is driven by structural factors, specifically the conversion economics of raw materials into battery-grade hydroxide.

Conflicts, Risks & Invalidation Watchpoints

A primary conflict exists between the bullish positioning reversal in lithium and the broader speculative crowding seen across other metals, which creates a risk of cross-sector contagion. Furthermore, the lack of fresh ETF creation suggests the market is currently vulnerable to "hollow" price moves. Our thesis weakens if the speculative z-score returns below its extreme short threshold of minus two, coupled with a reversal in flow momentum. A regime change to a renewed bearish state would be triggered by a significant spike in market volatility or a failure of the price to hold its 200-day support level during a macro-driven liquidation event.

Closing

In conclusion, the lithium market is transitioning out of an extreme short regime, supported by institutional deleveraging and a hardening of global supply chains. The mental model for this market should be one of a "fragile floor" where the lack of retail participation is being offset by a reduction in speculative selling pressure. We view the system as currently supported but fragile, awaiting a catalyst to translate this stabilization into a more robust trending regime.

All views expressed are personal, based on publicly available information, and do not represent the views of any employer or reflect any proprietary or internal analysis. This information should not be relied upon for making investment decisions.

No representation or warranty is made as to the accuracy, completeness, or timeliness of the information, and no liability is accepted for any loss arising directly or indirectly from its use.