Investor Anatomy Series

A structured, signal-driven synthesis of the gold market, integrating macro drivers, price behaviour, and institutional research into a single, decision-grade view.

Gold Outlook Podcast

Gold enters a tactical stabilization phase as structural liquidity expansion and US dollar weakness struggle to overcome a technical breakdown and cooling retail demand.

Executive Summary

Currently trading near the midpoint of its 52-week range following a nearly 20% drawdown, gold remains anchored by a structural liquidity expansion regime. While the dominant macro force is supportive, we maintain a cautious near-term bearish bias as the market works through a technical breakdown and institutional flow exhaustion.

Opening Thesis

The gold market is currently in a state of conflicted transition, where a robust macro backdrop is being challenged by a sharp deterioration in price momentum. While central bank accumulation and a broadening money supply provide a structural floor, the immediate reality is a system grappling with a removal of speculative sponsorship. We classify the current environment as a fragile balance, where the dominant force of liquidity expansion is being temporarily overridden by tactical liquidation. This matters because the path forward depends on whether the underlying macro tailwinds can re-assert control over a damaged technical structure.

Outlook

Over the next month, we anticipate a bearish bias as the market digests the recent breach of long-term trend lines. If the current technical breakdown persists without a reclaimed floor, we expect further consolidation toward the lower end of the annual range; however, if price stabilizes above recent lows, a tactical bottom may form. Looking out three months, the outlook shifts to bullish, provided that US dollar weakness and liquidity expansion continue to provide fundamental support. On a twelve-month horizon, we see a strong upward skew; if central bank diversification and fiscal concerns deepen as projected, gold is likely to trend toward institutional targets well above the five-thousand-dollar mark, though this remains contingent on real rates staying within a neutral band.

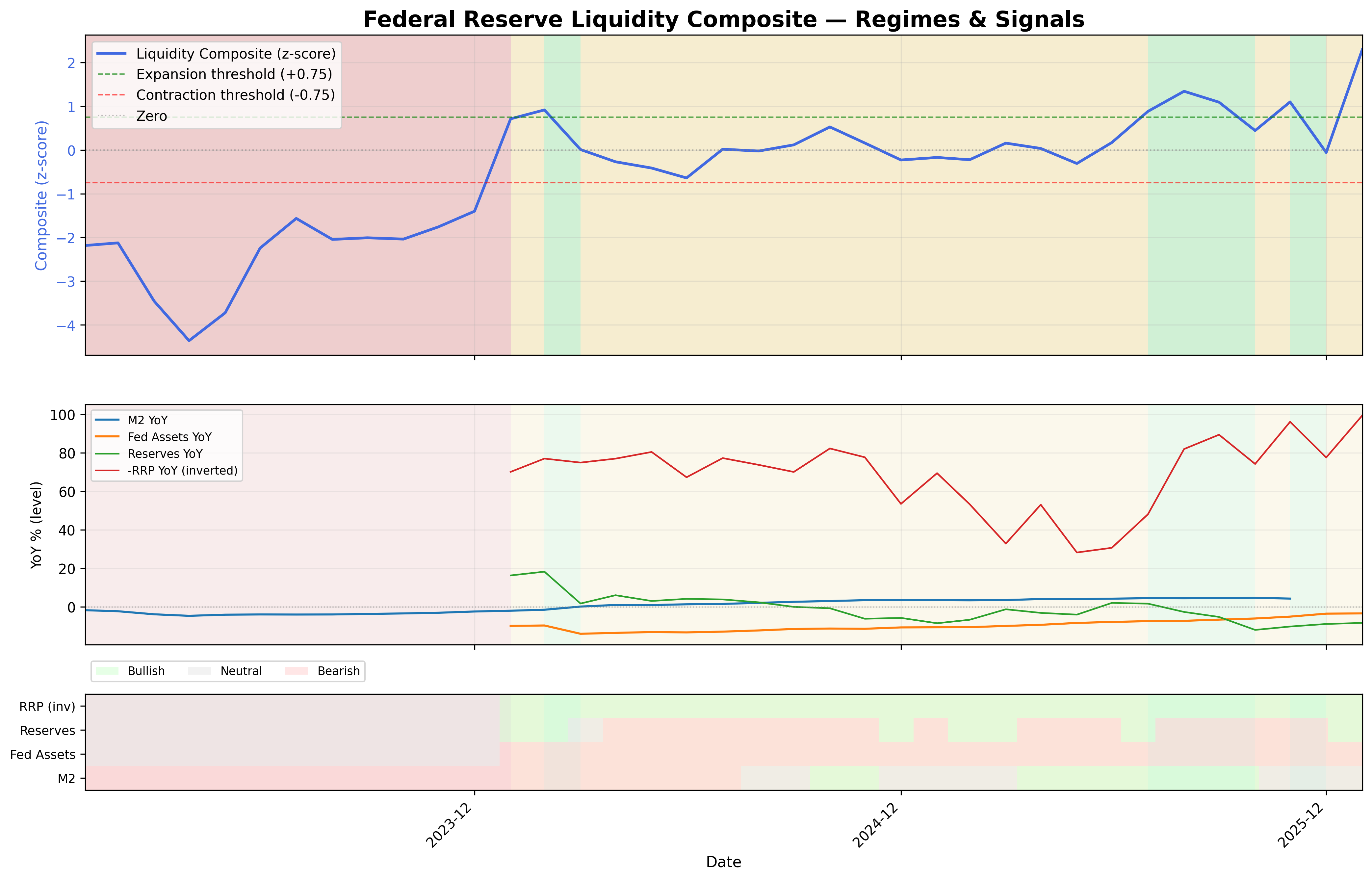

Market Regime and Macro Drivers

The market is currently operating under a regime of liquidity expansion, driven by a widening M2 money supply and a softening US Dollar Index. These forces act as the primary catalysts for gold's long-term value, yet they are currently meeting friction from high realized volatility and a neutral real interest rate environment. The causality here is clear: as global liquidity increases, the relative scarcity of bullion attracts capital, though this transmission is being hampered by a temporary cooling in risk appetite. Currently, the expansionary force of the macro backdrop dominates the long-term view, even as it is being overridden tactically by price volatility. We view the overall regime as a fragile balance, where the structural tailwinds are present but not yet fully expressed in price.

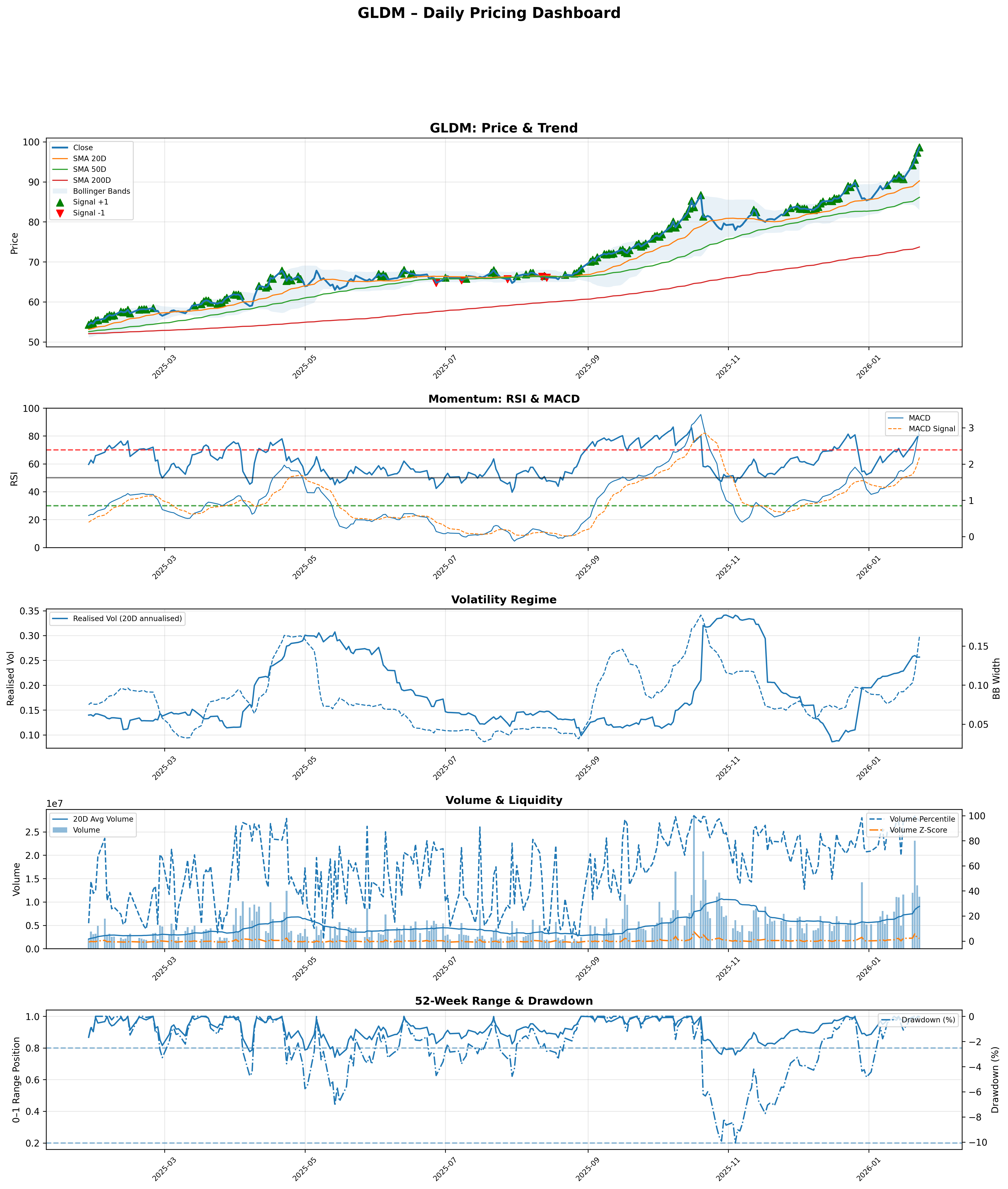

Price Action

Turning to the charts, gold’s recent behavior is defined by a significant breakdown below its 50-day and 200-day moving averages. With the GLDM proxy closing near eighty-five dollars, we have seen a nearly twenty percent drawdown from the 52-week high, placing price firmly in the midpoint of its annual range. We classify the current price regime as a technical breakdown following a period of high realized volatility. This behavior is actively resisting the broader macro regime, suggesting that the market requires a period of repair or a significant new catalyst to reclaim its former trending status.

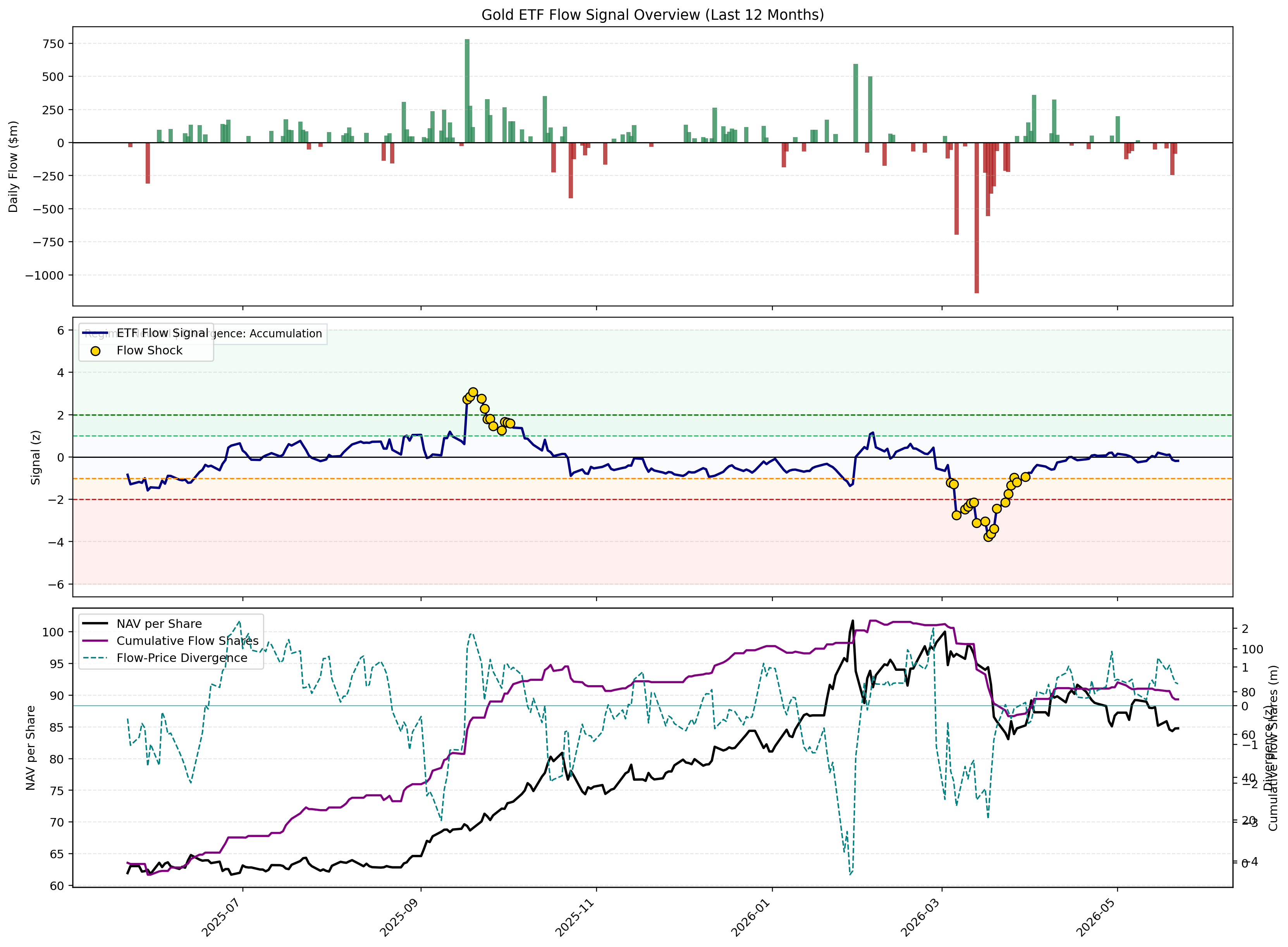

Market Expression and Capital Flows

Market expression reveals a stark divergence between different types of capital. ETF flows have entered a sustained outflow regime, with recent negative acceleration indicating a lack of conviction among institutional physical buyers. Conversely, the futures market shows a more nuanced picture; despite price weakness, we are seeing a bullish divergence in the Commitment of Traders data as speculators accumulate on dips. However, because the broader flow aggregate is negative and positioning remains fragile due to previous crowding, we conclude that capital is currently diverging from the supportive macro regime, creating a tactical headwind for price recovery.

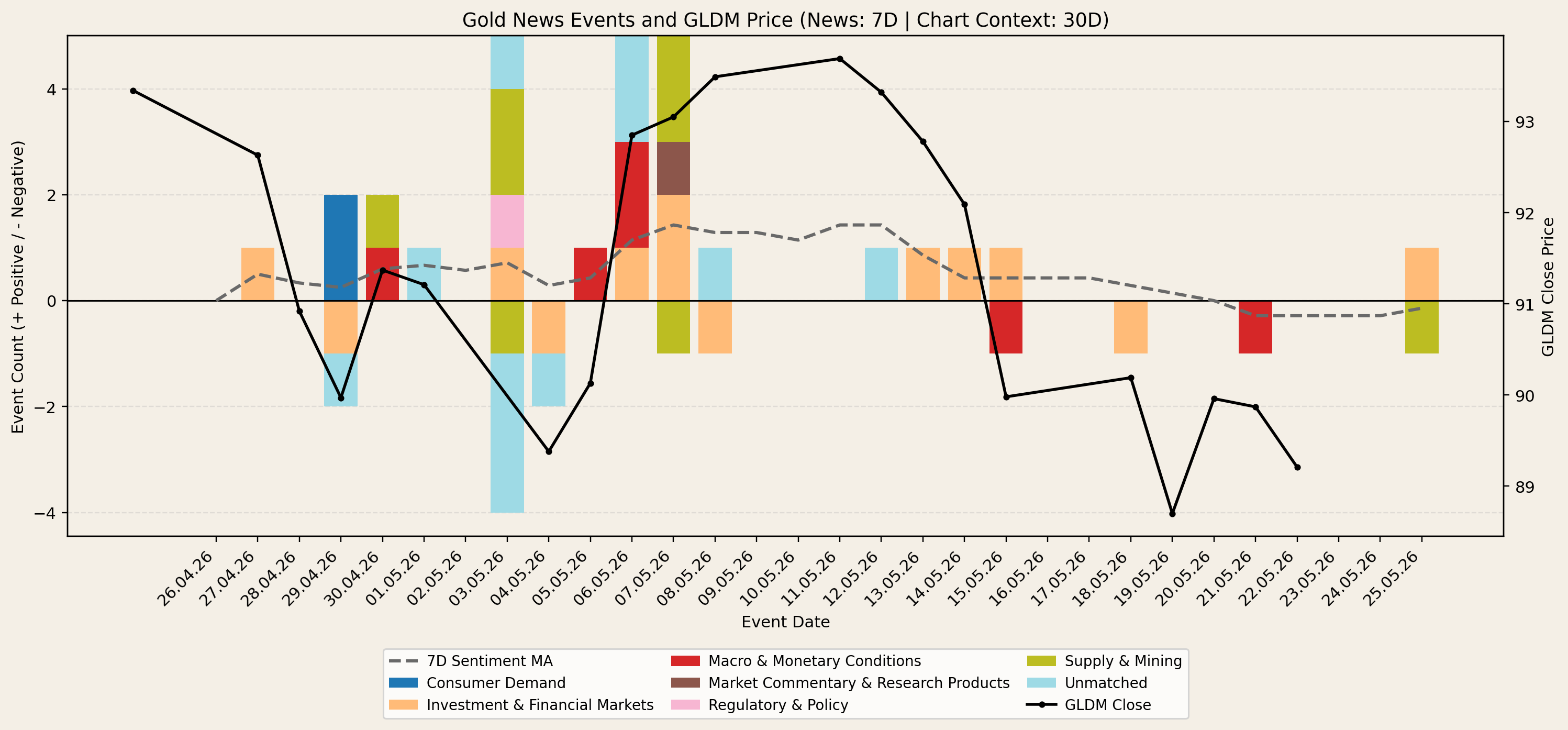

News Flow and Narrative

The narrative is shifting away from the speculative retail frenzy seen in Asia and toward more institutional themes, such as the debut of Fed Chair Kevin Warsh and the potential for geopolitical de-escalation regarding Iran. Markets are increasingly focused on how US monetary policy will react to supply-driven inflation and the long-term health of central bank reserves. We are also seeing a cooling in Chinese retail demand, which has historically been a major driver of momentum. Consequently, we view the current narrative as transitional, as it moves from a period of emotional retail participation to a more measured assessment of global macro policy.

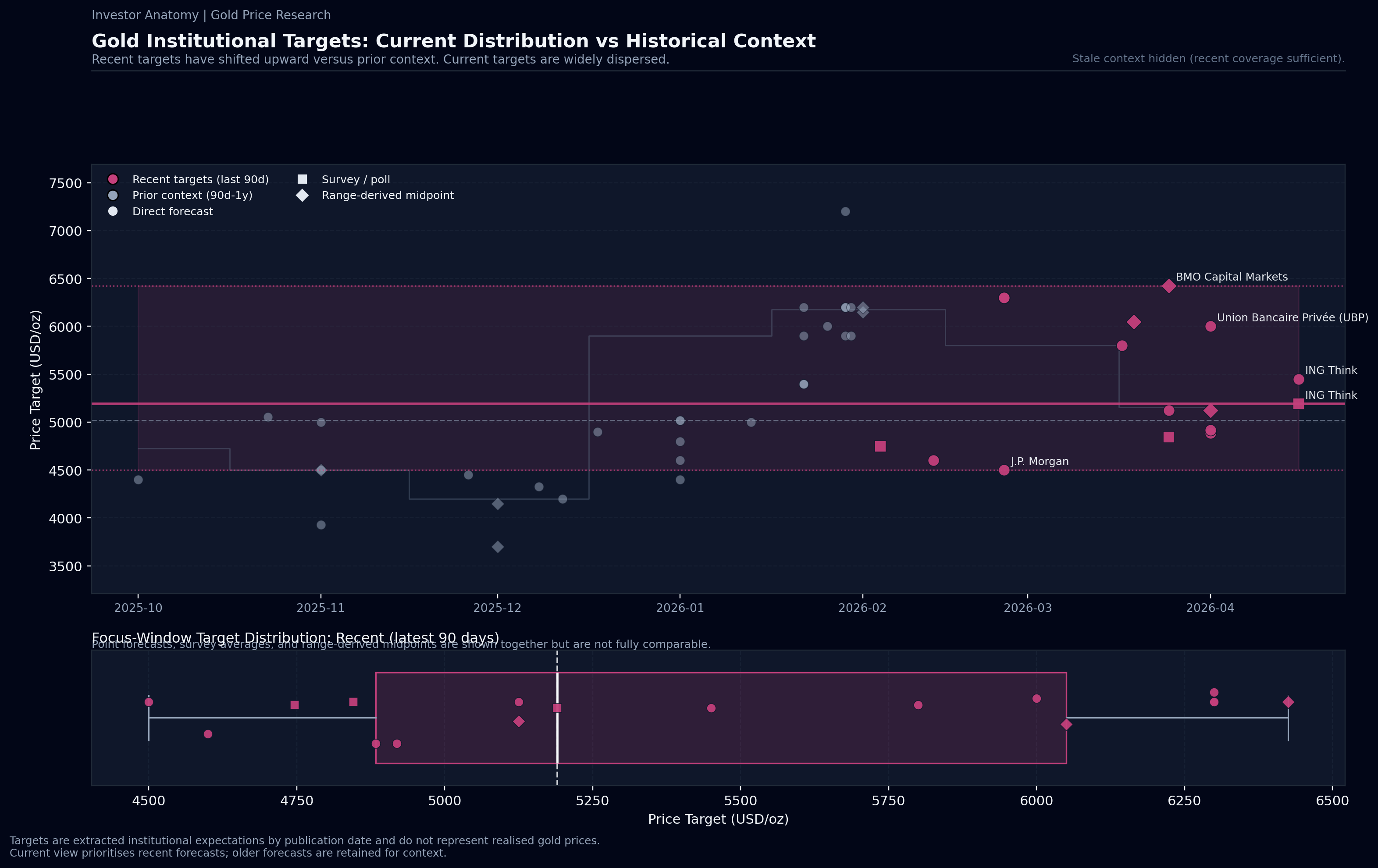

Target Pricing and Research

Institutional research anchors the market to a decisively higher price floor, with the median target for 2026 now sitting at five-thousand-one-hundred-and-twenty-five dollars. Our base case range extends from approximately forty-eight hundred to fifty-five hundred dollars, while more aggressive upside scenarios from firms like J.P. Morgan and UBS push as high as sixty-three hundred dollars. A stress or downside range is generally identified around the four-thousand-dollar level. Movement between these ranges is driven by structural shifts in central bank diversification and US fiscal trajectory, rather than short-term fluctuations in interest rate expectations.

Conflicts, Risks & Invalidation Watchpoints

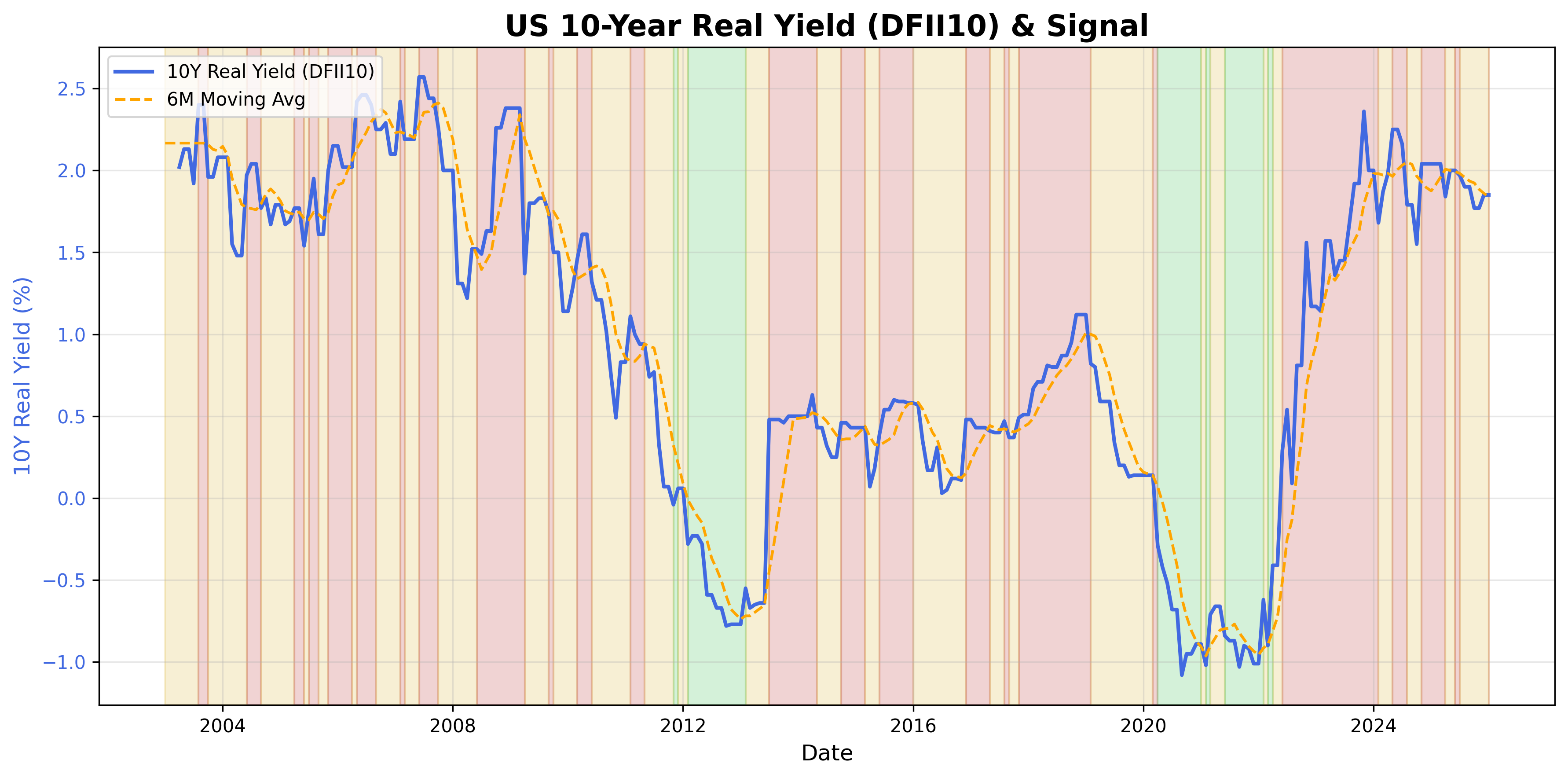

Several internal conflicts currently define the gold landscape, most notably the divergence between expansionary liquidity and contracting ETF flows. The primary risk is that gold continues to fail to express its macro tailwinds, suggesting a breakdown in the historical relationship between money supply and spot prices. We are closely monitoring two key triggers: if 10-year real yields sustain a move above neutral thresholds, the liquidity-driven bull case would be fundamentally invalidated. Furthermore, if the current technical breakdown leads to a breach of the four-thousand-dollar support level, we would view the entire structural regime as having transitioned from expansion to a more defensive or constrained state.

Closing

In summary, gold remains a market of two halves: a robust structural foundation of liquidity expansion and dollar weakness struggling against a damaged technical frame and institutional flow exhaustion. The mental model for the current market is one of a coiled spring that requires a stabilization of capital flows before the macro drivers can again dictate price. At present, we view the system as fragile, awaiting a clear signal that the tactical liquidation has run its course.

All views expressed are personal, based on publicly available information, and do not represent the views of any employer or reflect any proprietary or internal analysis. This information should not be relied upon for making investment decisions.

No representation or warranty is made as to the accuracy, completeness, or timeliness of the information, and no liability is accepted for any loss arising directly or indirectly from its use.