Copper Price Research

Institution-level institutional copper target extraction from IA researcher PDFs, with historical target tracking and synthesis.

Market Interpretation

Current Median Target

12,575.00

Recent (latest 90 days)

Current Target Range

12,000.00 - 14,500.00

Focus window min/max

Recent Forecast Count

8

Numeric rows driving current view

Median Shift vs Prior

↑ +575.00

Prior median: 12,000.00

Latest Publication

2026-04-21

Based on publication dates in the latest 90 days.

Comparability

High

Recent window is mostly direct institution forecasts.

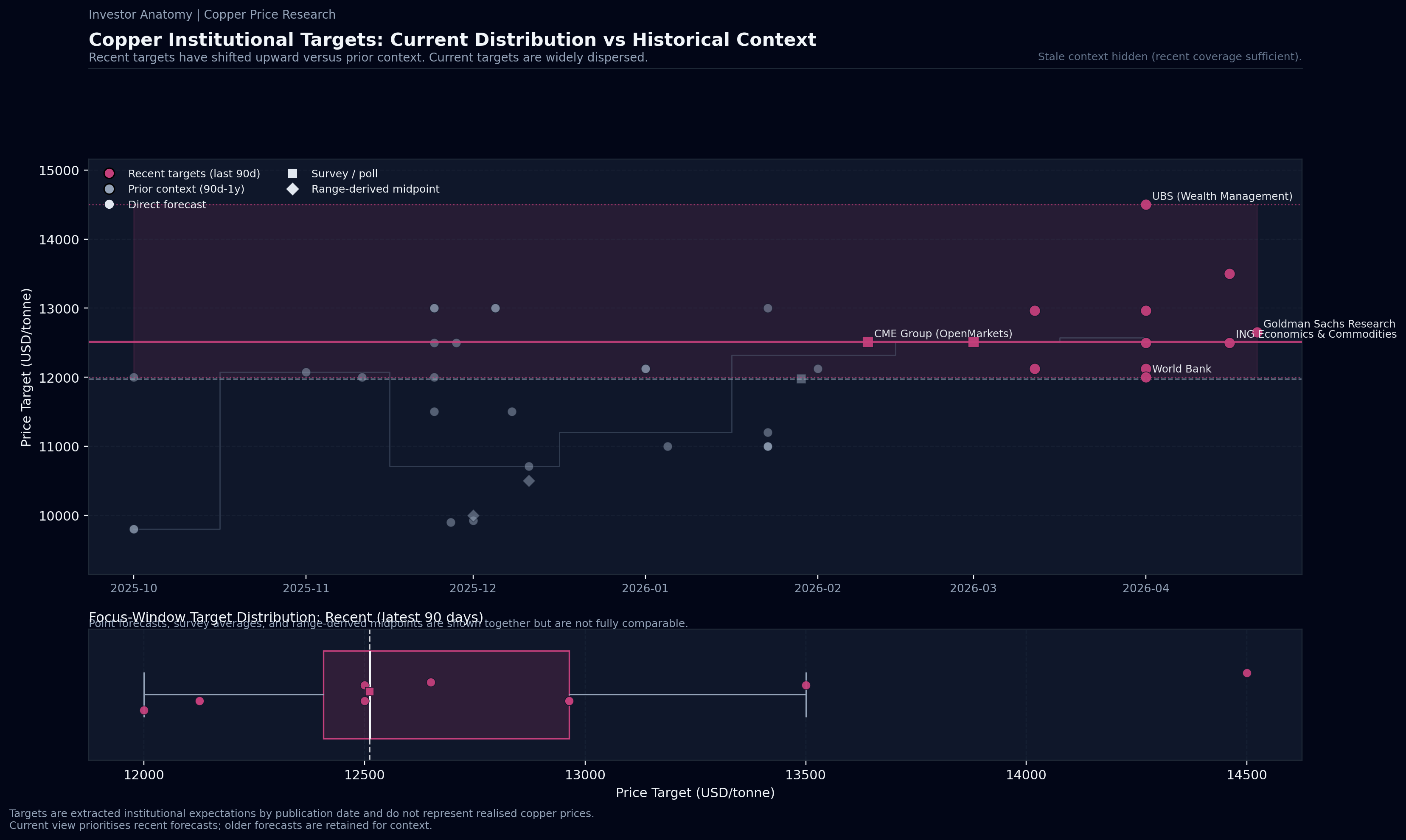

Current View: The institutional outlook for copper has shifted decisively upward in recent months, with the median price target for 2026 rising to $12,575 per tonne. This represents a significant strengthening of conviction compared to late-2025 projections, when the median sat at $12,000 per tonne. Most recent forecasts from major banks now converge in a higher bracket, signaling a market expectation that supply-side constraints and structural demand will sustain elevated price levels through the coming year.

Momentum and Drivers: Bullish sentiment is currently driven by a combination of acute supply risks—including disruptions in the Strait of Hormuz and mine-level constraints—and persistent demand from AI-driven data center infrastructure and global electrification projects. UBS Research recently provided the highest point forecast in the dataset at $14,500 per tonne for year-end 2026. Meanwhile, Goldman Sachs maintains a more nuanced profile, forecasting a peak of $13,000 in early 2026 before moderating toward $11,000 as supply-demand balances potentially normalize toward the end of the year.

Historical Trajectory: The distribution of targets has noticeably shifted upward as prior low-end anchors have been revised. Earlier assessments from the World Bank and RBC Capital Markets, which previously placed targets in the $9,800 to $9,920 range, have been superseded by updated estimates of $12,000 and $12,963, respectively. This migration suggests that the market deficit is increasingly viewed by institutions as a structural reality rather than a temporary cyclical spike.

Comparability and Conviction: While point forecasts from major investment banks are tightly clustered above $12,000, broader market aggregates show a slightly more conservative outlook. A Reuters poll of 30 analysts reported a consensus average of $11,975 per tonne, indicating that while lead institutions are highly bullish, a segment of the broader analyst community remains cautious about the sustainability of prices exceeding $13,000. Fundamental context from the International Copper Study Group (ICSG) supports the bullish narrative, projecting a transition from a 2025 surplus to a 150 kt deficit in 2026.

Mixed Signals and Risks: Despite the prevailing upside bias, there is mixed conviction regarding the latter half of 2026. Institutions such as ING Research and Goldman Sachs suggest a "front-loaded" price path, where Q2 2026 acts as a peak followed by a softening toward the $11,000–$11,500 range. This anticipated cooling is attributed to potential demand destruction at record price levels, increased scrap supply, and the fading of tariff-related stockpiling uncertainty that is currently inflating short-term inventory requirements.

Outlook Summary: The current data reflects a consensus that is tightening at higher price levels for the first half of 2026, underpinned by specific geopolitical and infrastructure catalysts. However, the outlook remains dispersed for the long term, as analysts weigh the competing forces of structural electrification demand against the likelihood of a supply response or a slowdown in Chinese industrial activity. Overall, the distribution of targets implies a strong upside bias relative to the historical record.

Target Visuals

Recent forecasts are emphasised; older retained forecasts provide historical context. Targets represent extracted institutional expectations, not realised copper prices.

Extracted Data (Validation)▸

All views expressed are personal, based on publicly available information, and do not represent the views of any employer or reflect any proprietary or internal analysis. This information should not be relied upon for making investment decisions.

No representation or warranty is made as to the accuracy, completeness, or timeliness of the information, and no liability is accepted for any loss arising directly or indirectly from its use.