Investor Anatomy Series

A structured, signal-driven synthesis of the copper market, integrating macro drivers, price behaviour, and institutional research into a single, decision-grade view.

Copper Outlook Podcast

The copper market has entered a tactical consolidation phase as expansionary macro tailwinds face a significant retreat in speculative sponsorship and mounting realized volatility.

Executive Summary

With prices currently holding near 52-week highs despite recent momentum cooling, the market is navigating a sharp conflict between supportive global liquidity and a bearish reversal in capital flows. We maintain a neutral bias for the immediate term as the market seeks a floor, though the underlying structural deficit remains the primary directional anchor for 12-month institutional projections.

Opening Thesis

We are currently observing a market in transition, where the aggressive rally of late spring is being tested by a tactical withdrawal of speculative capital. While global growth signals and expansionary monetary conditions continue to provide a structural tailwind, they are currently being overridden by a bearish reversal in positioning. This shift is significant because it signals a move away from momentum-driven price discovery toward a regime of high-volatility consolidation. At present, speculative liquidation is the dominant force, keeping the overall analytical system in a state of fragile balance.

Outlook

Over the one-month horizon, if speculative liquidation persists without a fresh industrial catalyst, we expect prices to drift lower toward primary support levels as momentum remains suppressed. Looking out three months, if global liquidity expansion continues and the US dollar remains in its current weakening trend, copper should resume its upward trajectory as cyclical demand reasserts itself over tactical positioning. On a twelve-month basis, if the projected transition from a market surplus to a 150-kilotonne deficit materializes, we anticipate a structural breakout toward record institutional price targets. Conversely, if global growth indicators breach expansionary thresholds or real rates move sharply higher, the strategic bull case will likely be deferred in favor of a deeper mean reversion.

Market Regime and Macro Drivers

The current regime is defined by a powerful expansionary liquidity backdrop that is acting as a floor for the industrial metals complex. This tailwind is primarily driven by a weakening US dollar and a favorable global growth impulse, which traditionally incentivizes pro-cyclical positioning. However, these forces are currently navigating an environment of elevated volatility, which acts as a near-term constraint on trend extension. We find that while liquidity is the structural anchor, it is being temporarily overridden by tactical de-risking in higher-beta assets. Consequently, we characterize the overall regime as a fragile balance, where the long-term macro tailwind is present but currently lacks the momentum to overcome short-term capital outflows.

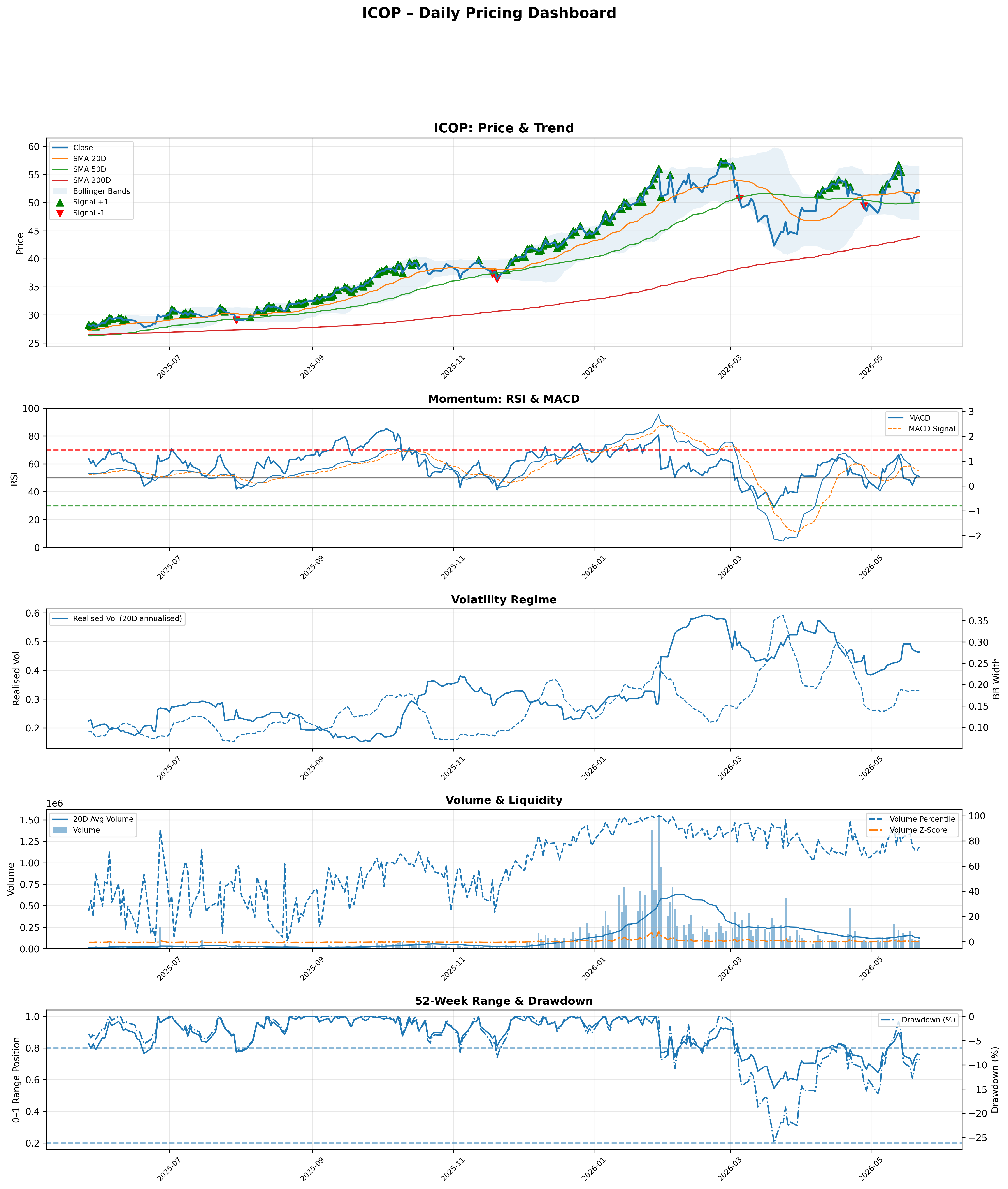

Price Action

Price behavior is currently reflecting a failed breakout attempt that has evolved into a high-volatility consolidation. Although the market remains positioned above both the 50-day and 200-day moving averages—a technical hallmark of a long-term bull trend—the recent retreat from the 52-week highs indicates a loss of immediate upward thrust. With realized volatility sitting in the 85th percentile, the current price regime is best described as range-bound with a defensive lean. The interpretation here is one of resistance; price is not currently confirming the macro tailwind, suggesting that a period of base-building or further drawdown is required before a clean trend extension can be sustained.

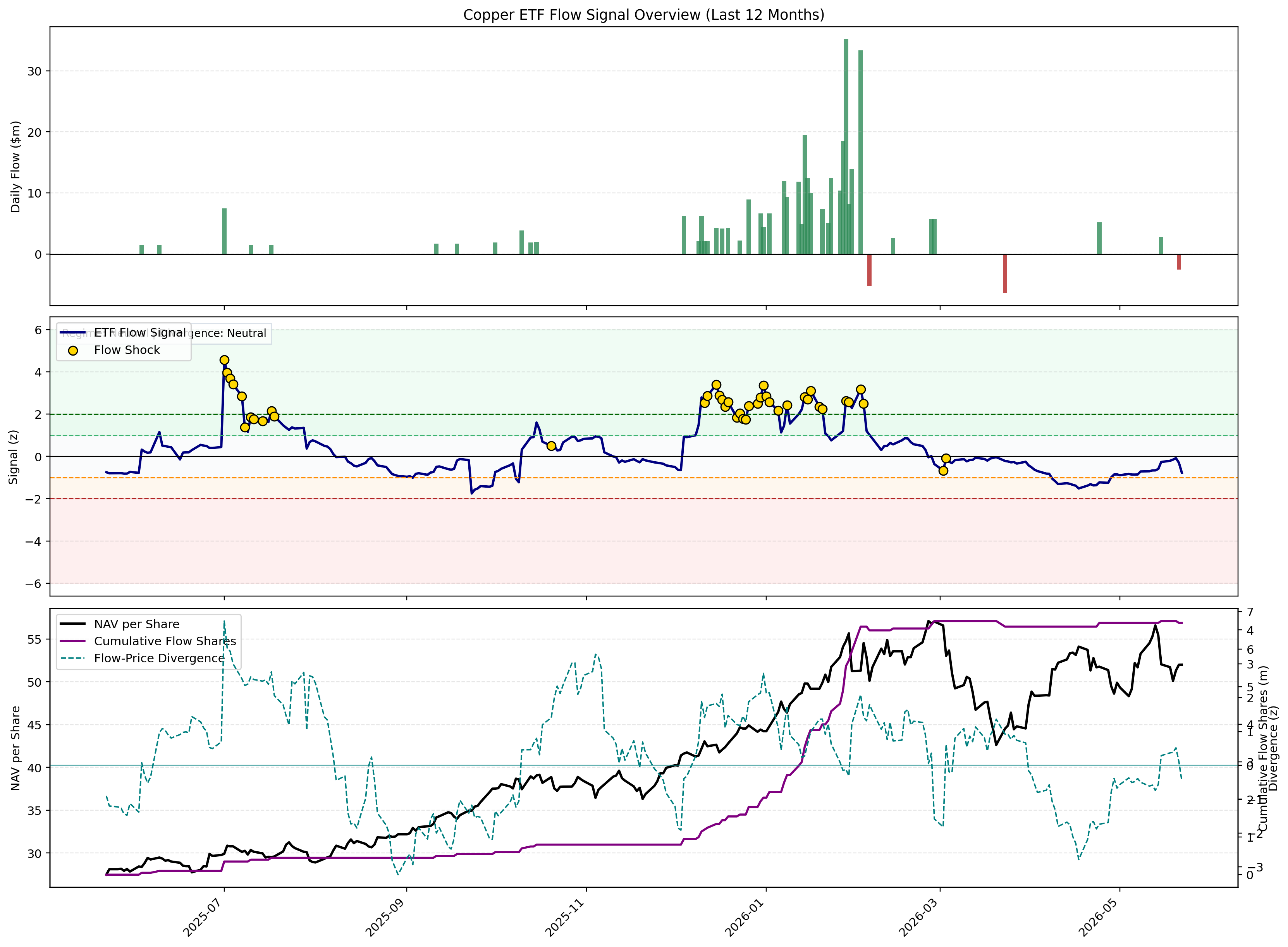

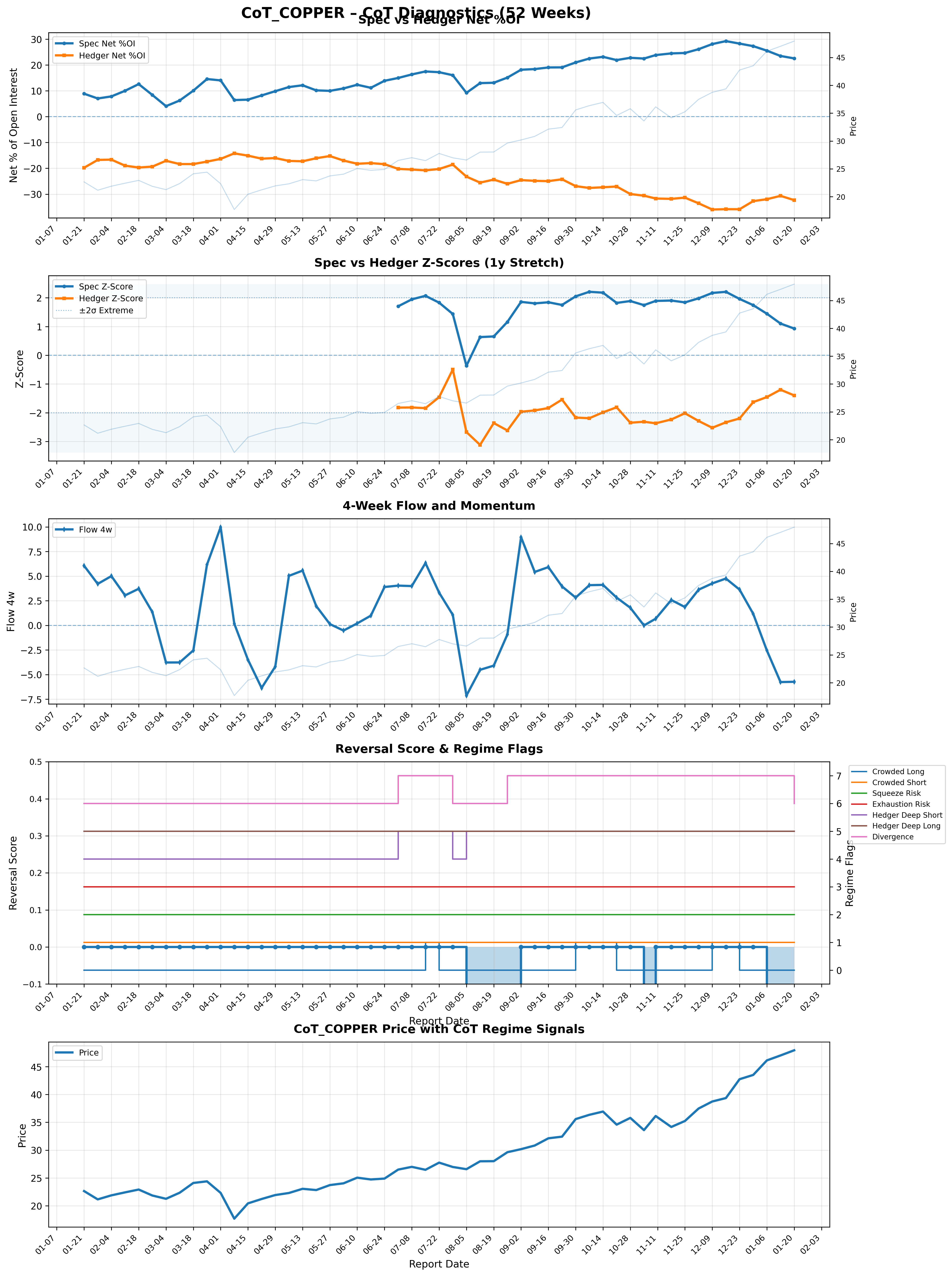

Market Expression and Capital Flows

Capital flows are currently diverging from the broader macro regime, suggesting a lack of institutional conviction at these elevated levels. Speculative positioning has seen a sharp reversal, with 4-week flows turning significantly negative as traders liquidate long exposure. This is mirrored in the ETF space, where recent aggressive outflow pressure has only just stabilized into a neutral regime. While positioning is not yet at the extreme "crowded short" levels that would typically trigger a squeeze, the current z-score indicates that the market is shedding the exuberance seen earlier in the quarter. We conclude that capital expression is neutral to diverging, providing no immediate sponsorship for a renewed rally.

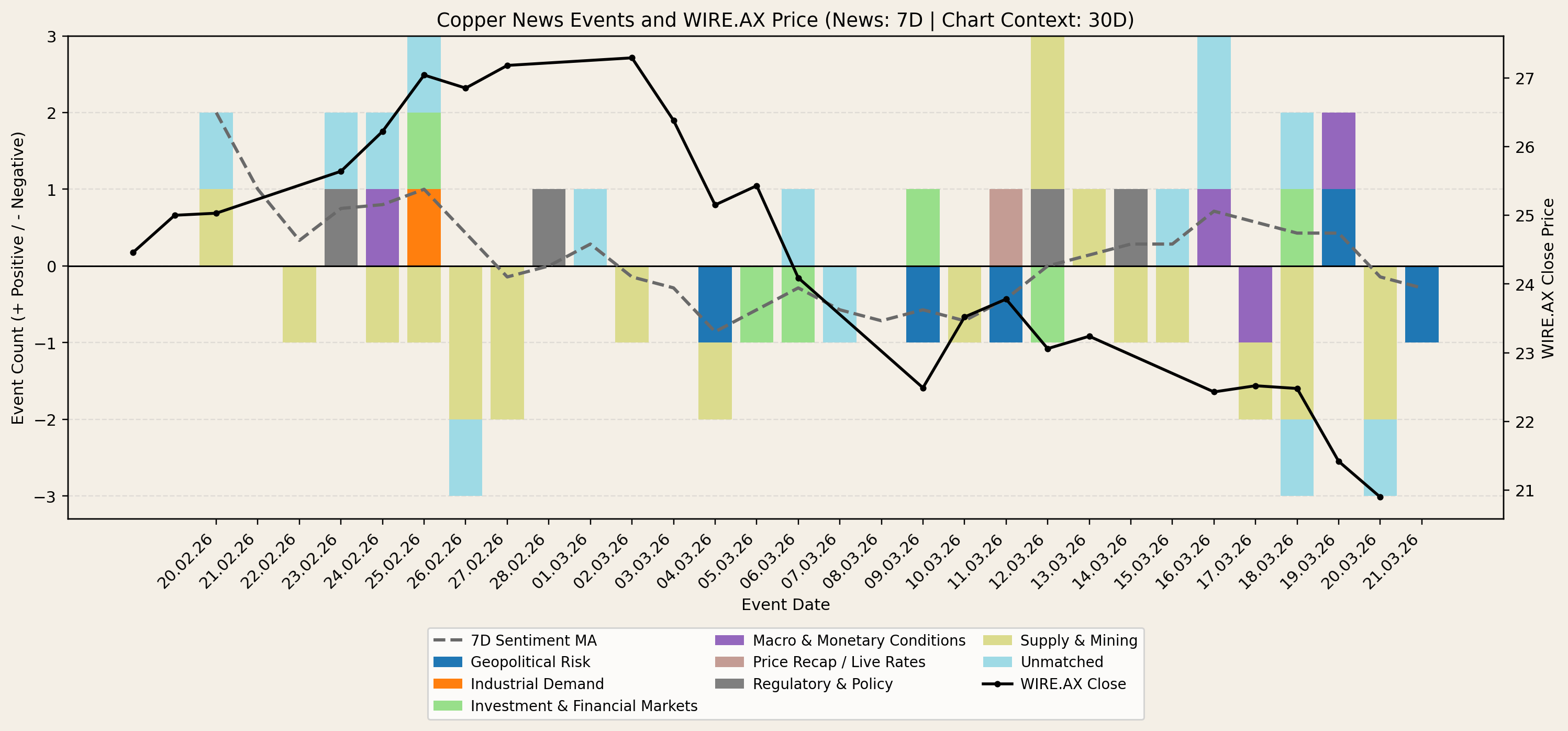

News Flow and Narrative

The copper narrative is undergoing a transition from immediate geopolitical risk-off sentiment toward a focus on long-term supply sustainability. We are seeing three dominant themes: the formalization of trade sanctions on Russian-origin material, persistent localized disruptions in major mining jurisdictions, and a significant upward revision in the valuation of future North American projects. While de-escalation in certain conflict zones has removed some of the energy-driven inflation premium, the market is now fixated on the "hunt for profits" among smelters facing a tightening concentrate market. This narrative is ultimately reinforcing for the strategic bull case but remains transitional in the near term, as it highlights that supply is becoming the defining constraint over temporary macro shocks.

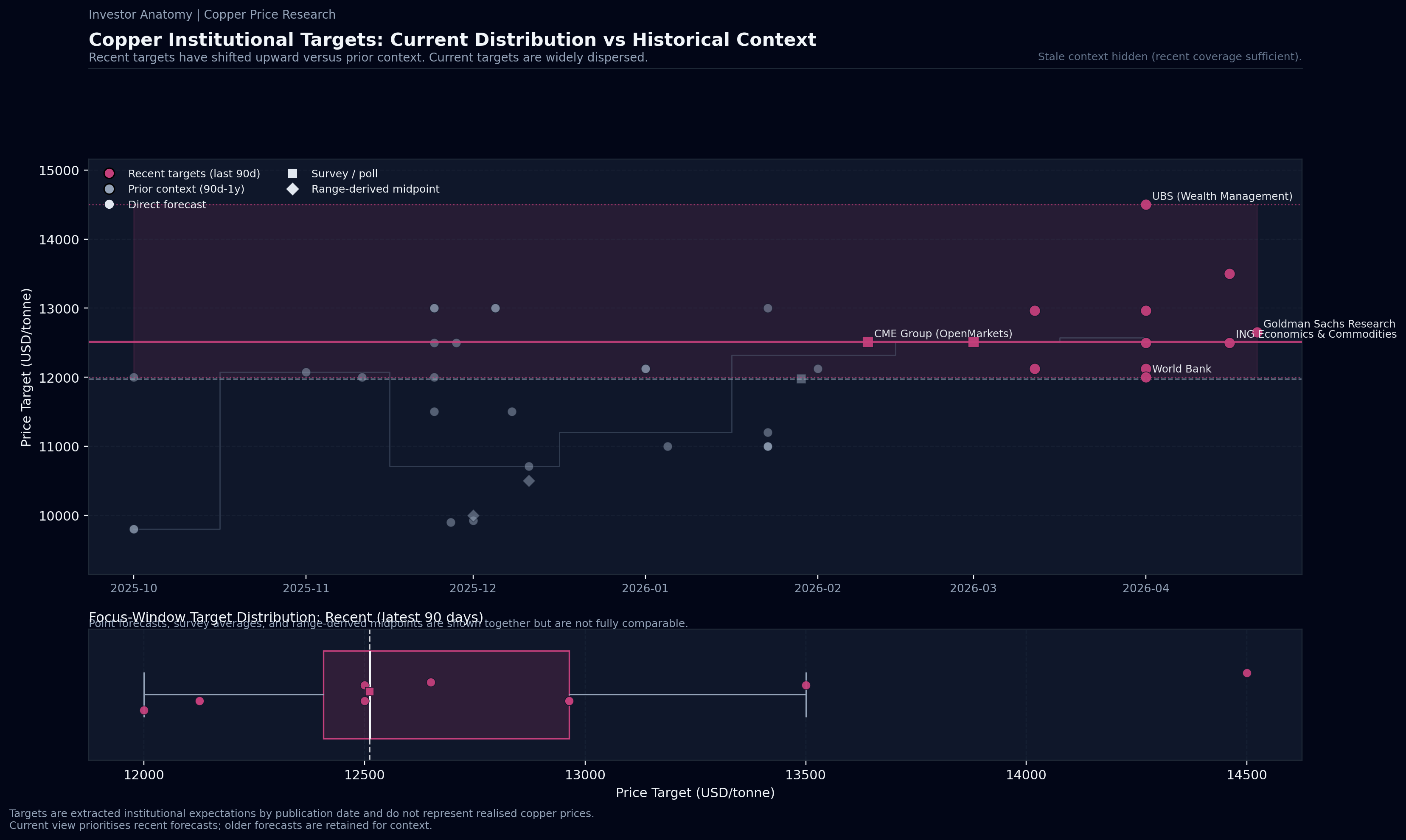

Target Pricing and Research

Institutional research has established a decisively bullish anchor, with the median target for the next twelve months rising to 12,575 dollars per tonne. Our base case range resides between 12,000 and 13,500, supported by the anticipated transition to a structural market deficit in 2026. An upside scenario, reaching as high as 14,500, is predicated on acute supply shocks or a non-linear acceleration in AI-driven grid infrastructure demand. On the downside, a stress range of 10,500 to 11,000 would likely be triggered by a collapse in global industrial demand or a significant over-rotation of real interest rates. The migration of targets toward the upper bound suggests that the market now views high copper prices as a structural reality rather than a cyclical anomaly.

Conflicts, Risks & Invalidation Watchpoints

The primary conflict in our system is the disconnect between expansionary macro signals and negative speculative flows. Currently, the technical and macro tailwinds are being overridden by tactical exhaustion in the metals complex. A critical invalidation watchpoint is the US Dollar Index; if the dollar moves into a sustained strengthening regime, the current tailwind thesis will be broken. Furthermore, we are monitoring for a speculative Z-score drop below negative 2.0, which would transition the risk profile from long liquidation to an acute short-crowding event. Market structure risks also include the potential for demand destruction if prices sustain levels above 13,000, which could invite a surge in scrap supply and invalidate the deficit projection.

Closing

In summary, copper is currently a market catching its breath after a period of intense speculative fervor. The mental model for the current environment is one of macro support meeting tactical fatigue—the long-term structural foundations are solid, but the near-term capital dynamics are currently unsupportive. Consequently, we view the system as constrained and fragile, requiring a stabilization of positioning or a fresh fundamental catalyst before the broader bullish regime can reassert its dominance.

All views expressed are personal, based on publicly available information, and do not represent the views of any employer or reflect any proprietary or internal analysis. This information should not be relied upon for making investment decisions.

No representation or warranty is made as to the accuracy, completeness, or timeliness of the information, and no liability is accepted for any loss arising directly or indirectly from its use.